Stock of the Week: Is Apple’s Reign at the Top Under Threat?

Is market confidence in Apple still justified?

Here is the 18th edition of “Stock of the Week”. You can find all the previous analyses and my articles on my main page (for an easier search, use a computer, mobile version is harder to navigate).

Here are the links to the 3 previous “Stocks of the Week” as well

This week, we are focusing on Apple. Despite its lofty valuation and slowing growth, Apple has managed to hold its ground. But with rising political risks (like Trump’s recent threats) can that resilience continue? Let’s take a closer look!

How do you view Apple’s current position? Share your perspective below

While free subscribers already benefit from a wealth of valuable content, upgrading to a paid subscription unlocks exclusive research, in-depth insights, real-time portfolio tracking, advanced stock screeners, and more giving you an edge to stay ahead of the market. Don’t miss out: subscribe now and supercharge your investing journey!

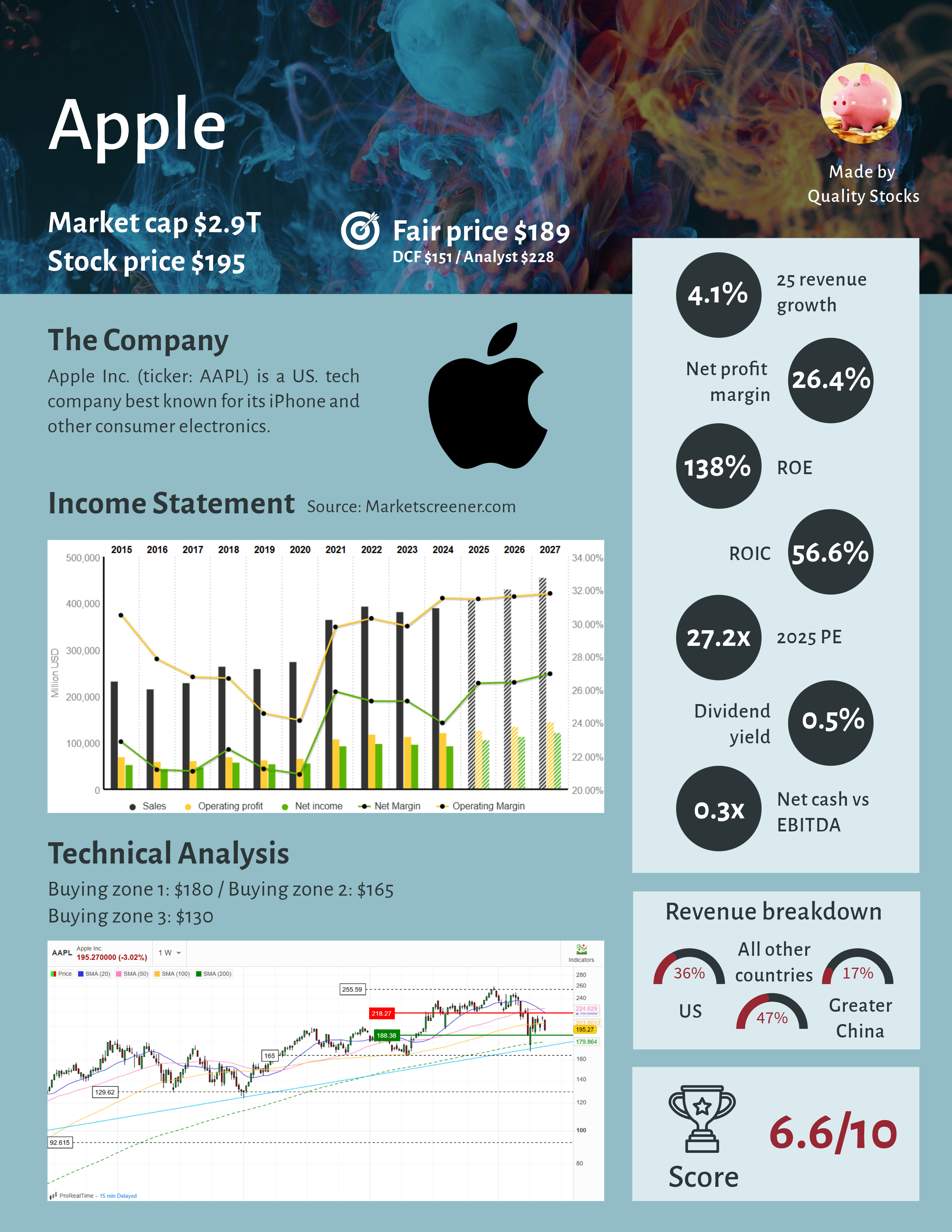

One Pager

The stock at a glance!

Recent news

President Trump’s criticism of Apple’s move to shift iPhone production to India highlights growing tariff tensions and his push for US-based manufacturing. He threatened to impose 25% tariffs

Despite mounting political pressure, Apple is doubling down on its India manufacturing strategy with no plans to scale back investments

Apple’s dependency on China for manufacturing (accounting for roughly 90% of iPhone current production) exposes it to geopolitical risks

Apple appears to be lagging in the AI race, with internal reports pointing to slow progress and ongoing struggles, particularly with Siri, whose limitations may undermine Apple’s long-term product strategy

While innovation and rising competition have loomed as threats for years, Apple has managed to maintain its dominance. However, concerns are growing as the company reportedly considers raising iPhone prices this fall, banking on new feature upgrades to justify the increase

For now, Apple’s services segment is the key driver of growth and margins, growing over 11% and accounting for 25% of total revenue

Last earnings report

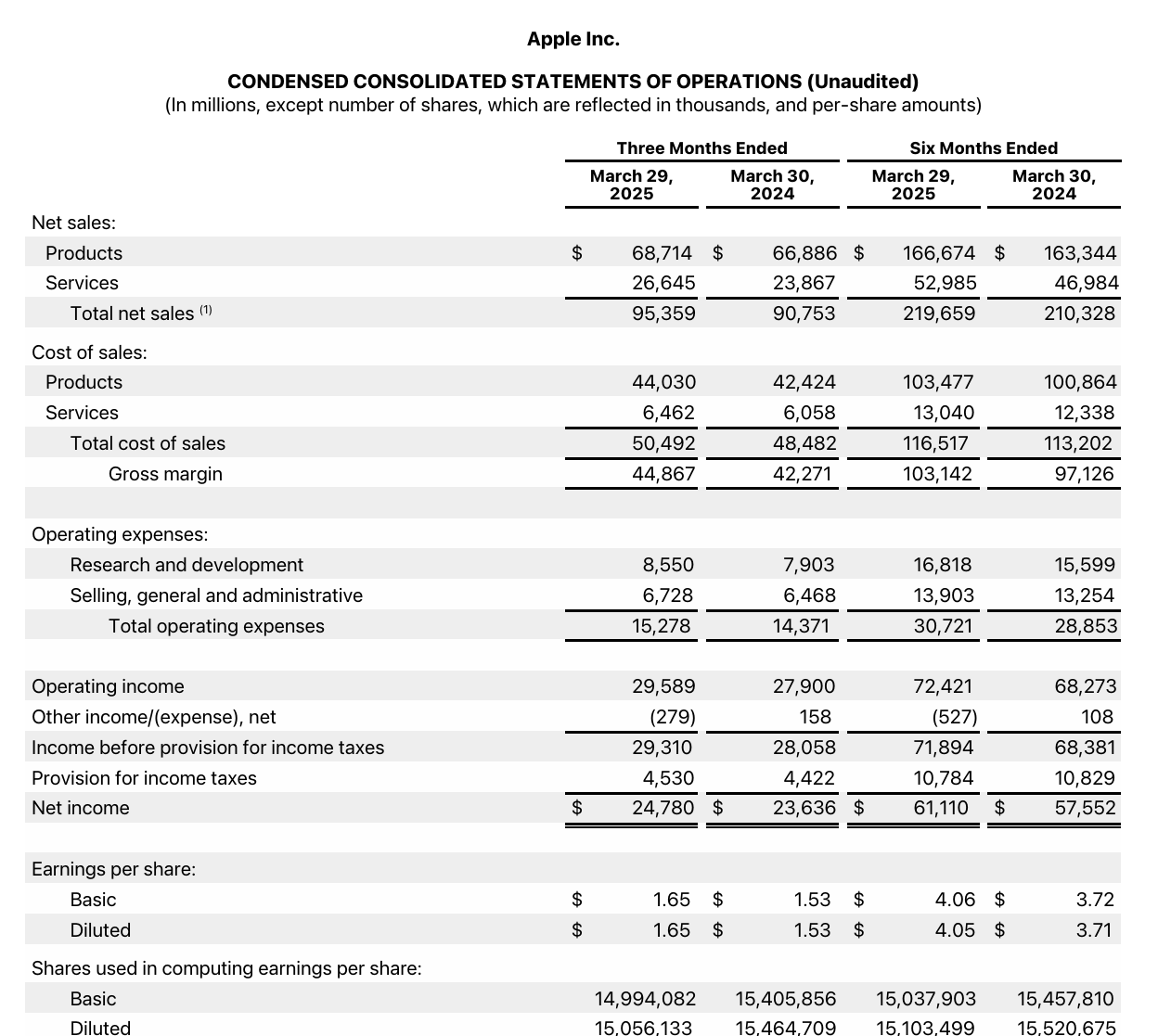

Apple reported $95.4B in revenue for the quarter, marking a 5% YoY increase, while EPS rose 8%. By segment, iPhone revenue edged up 2%, and services revenue posted a strong 11% gain.

The company also unveiled plans for a $500B US investment over the next 4 years, which includes the construction of a new server factory in Texas. CEO Tim Cook highlighted the continued momentum in services and teased upcoming launches like the new iPhone and next-gen Macs and iPads powered by Apple Silicon. CFO Kevan Parekh underscored the solid EPS growth and commitment to shareholder returns, even as the company navigates tariff headwinds and ongoing challenges in AI development.

Analysts’ recommendations

May, 13. Daiwa. Buy. $270 —> $240

May, 12. China Renaissance. Buy. $248 —> $239

May, 5. CICC. Buy. $285 —> $260

May, 5. Phillip Securities. Hold. $235 —> $200

May, 2. Bank of America. Buy. $240 —> $235

May, 2. Monness Crespi $ Hardt. Buy. $260 —> $245

May, 2. Citigroup. Buy. $245 —> $240

May, 2. BNP. Hold. $180 —> $190

May, 2. TD Cowen. Buy. $290 —> $275

May, 2. DA Davidson. Buy. $290 —> $250

May, 2. Goldman Sachs. Buy. $256 —> $253

May, 2. Wedbush. Buy. $250 —> $270

May, 2. Baird. Buy. $260 —> $230

My analysis

Despite the current turbulence, Apple remains one of the most powerful (if not the most powerful) brands globally. Its enduring strength stems from a tightly integrated ecosystem and a brand universe that has been carefully cultivated over many years

The company’s robust growth in services revenue (characterized by high margins and recurring income) is a direct reflection of that ecosystem. This segment has become a crucial engine for both profitability and resilience

However, Apple faces a growing set of challenges: tariff risks, geopolitical tensions, intensifying competition, a perceived lag in AI innovation and questions around its pricing power. Many of these risks may not yet be fully reflected in the stock’s valuation

That said, Apple is far from defenseless. Its immense cash flow and industry-leading profitability give it significant firepower to invest in emerging technologies and adapt strategically

Given the current valuation and risk backdrop, a prudent long-term investor might prefer to wait for a more attractive entry point, one that offers a greater margin of safety

Technical analysis

I have defined three buying zones that I find interesting for long-term investments during pullbacks. While these zones may not be reached, I am prepared for a market (or stock) consolidation to seize long-term opportunities. For me, this approach offers a better risk/reward ratio.

Of course, this is just my opinion, and I am sharing it with you, but each investor should decide on their own investment style. With that said, here are my three buying zones for Apple.

Buying zone 1. $180

Buying zone 2. $165

Buying zone 3. $130

If you enjoyed this article and like Quality Stocks, please give it a like and spread the word!

Used source: Marketscreener.com. Affiliate link just here