Stock of the Week: Transmedics - Cutting Through the Controversy

Earnings beat drowns out short seller doubts

Here is the 16th edition of “Stock of the Week”. You can find all the previous analyses and my articles on my main page (for an easier search, use a computer, mobile version is harder to navigate).

Here are the links to the 3 previous “Stocks of the Week” as well

This week, we are focusing on Transmedics. The company, a leader in organ transplant technology and services, delivered outstanding earnings that sent its stock soaring over 20%. Let’s dive in!

What are your thoughts on Transmedics? Share them in the comments!

While free subscribers already benefit from a wealth of valuable content, upgrading to a paid subscription unlocks exclusive research, in-depth insights, real-time portfolio tracking, advanced stock screeners, and more giving you an edge to stay ahead of the market. Don’t miss out: subscribe now and supercharge your investing journey!

One Pager

The stock at a glance!

Recent news

One of the biggest recent developments for Transmedics was a short seller report released in early 2025. I published a detailed analysis of that report, which you can read if you are interested in a deeper dive.

In that article, I broke down the short seller report and shared my conclusions. Out of the 3 possible scenarios I considered, the most likely one was this “Despite rising competition, the company's value proposition remains strong, and it manages to grow. It is common for early-stage companies to face challenges, make mistakes, and experience both successes and failures. In this scenario, the company will improve while continuing to grow and future reports will likely be positive.”

In short, I was not convinced by the short seller’s claims. That said, I am staying cautious because in markets, you can never be too sure.

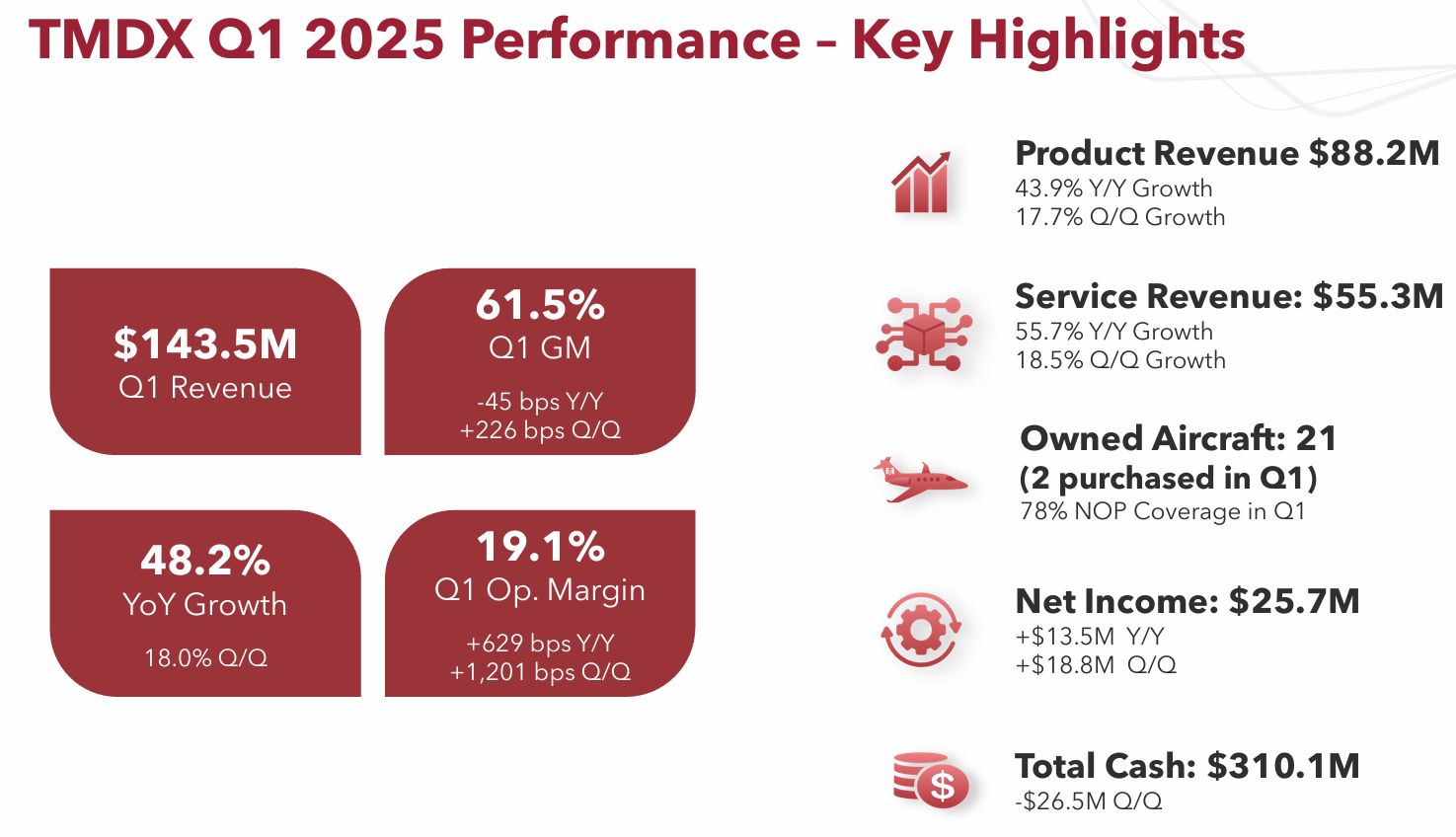

Last earnings report

Transmedics reported a record revenue of $143.5M, up 48% YoY, with net income margin rising from 13% to 18%.

Analysts expected revenue to reach $123M, reflecting 27% YoY expected growth, but the real standout was the margin expansion. EPS were projected at $0.25, yet Transmedics delivered $0.70, nearly tripling expectations and doubling from a year ago.

Service revenue grew faster (56% YoY) than product revenue (44% YoY) and the company continued to purchase new aircrafts for its logitics.

With this strong start of the year the company increased its FY 25 guidance from $530M - $552M revenue to $565M - $585M revenue.

My analysis

TransMedics is showing strong momentum, driven by robust revenue growth and significant margin expansion, an encouraging setup for continued outperformance.

For now, the short seller report has largely faded from the market’s attention, though it could resurface. While many of its claims appeared exaggerated, a few points could still raise valid concerns.

The primary question now lies in valuation. The stock has nearly doubled from its recent lows just a month ago. If the company continues to execute at this level, the current price may be justified, but chasing the rally could be risky. A prudent investor might consider waiting for a potential pullback or consolidation before entering a position.

Technical analysis

I have defined three buying zones that I find interesting for long-term investments during pullbacks. While these zones may not be reached, I am prepared for a market (or stock) consolidation to seize long-term opportunities. For me, this approach offers a better risk/reward ratio.

Of course, this is just my opinion, and I am sharing it with you, but each investor should decide on their own investment style. With that said, here are my three buying zones for Transmedics.

Buying zone 1. $80

Buying zone 2. $57

Buying zone 3. $38

If you enjoyed this article and like Quality Stocks, please give it a like and spread the word!

Used source: Marketscreener.com. Affiliate link just here