Almost a year ago, I published this article with a deep dive on Zoetis (ticker: ZTS), the leader in animal health.

After a decent growth in 2024 (+8% vs 2023), analysts only expect 1% growth in 2025. Why? Is the company in a bad situation? Let’s find out!

Last earnings report

For the Q4 24 2024, Zoetis reported revenue of $2.3B, reflecting a 5% increase compared to the same period in 2023. On an operational basis (excluding foreign exchange impacts), revenue grew by 6%. Net income for the quarter was $581M, up 11% from Q4 2023, or $1.29 per share, a 13% increase.

For the full year 2024, Zoetis reported total revenue of $9.1 billion, a 6% increase from 2023. Net income for the year reached $2.5B, or $5.47 per share, up 5% and 7%, respectively.

US revenue rose 11% to $5.1B, while international revenue grew 2% to $4.1B.

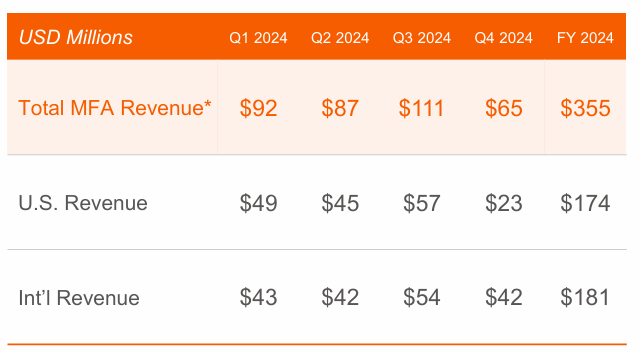

The Medicated Feed Additive (MFA) divesture

At the end of Q3 24, Zoetis completed the divesture of its MFA product portfolio to Phibro Animal Health. The goal was to streamline the company’s portfolio, to increase operational focus, prioritize faster growing business lines with higher margin and more innovation.

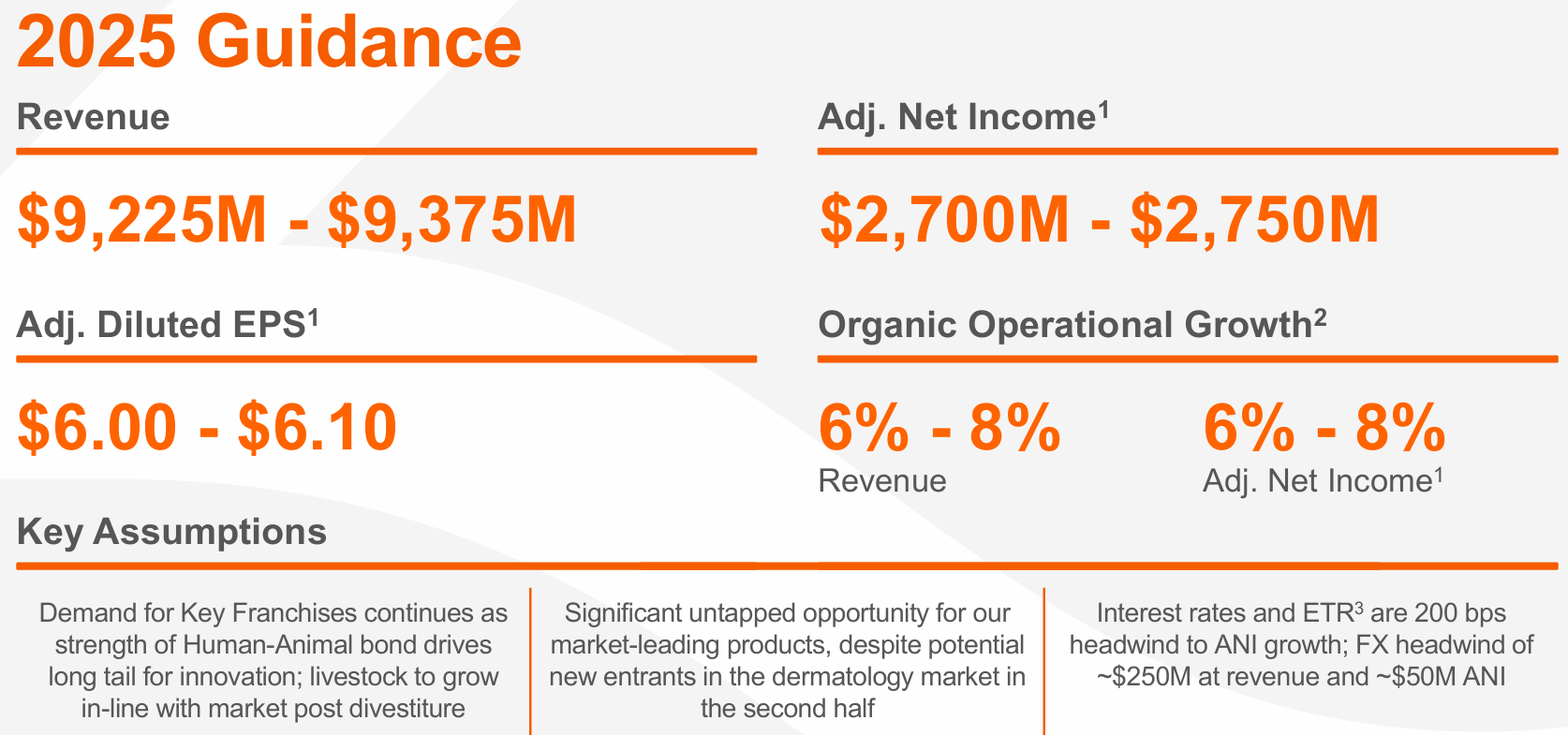

The guidance

While the guidance came in below expectations ($9.57B in revenue and $6.30 EPS), this is primarily due to the divestiture we just discussed. Excluding this impact, organic revenue growth is projected to remain robust, in the 6% to 8% range, broadly in line with the company’s historical performance and with my assumptions based on the market growth and market share gains.

Analysts now forecast the following annual revenue figures:

2025 $9,362M (+1.1%)

2026 $9,978M (+6.6%)

2027 $10,548M (+5.7%)

This future growth is fueled by a robust pipeline.

The company remains focus on key elements we like to see as investors:

Growing above the market growth (therefore gaining market share)

Investing in innovation and prioritizing highest ROIC opportunities

Increasing net income faster than revenue (therefore increasing margin)

Returning excess capital to shareholders through share buybacks and dividends

In the rest of the article, I revise my fair value to account for the growth slowdown, pinpoint strategic buy zones, and break down the potential upside for investors buying in today.

Want the full breakdown? Unlock it and all my content by joining as a paid subscriber!