Fortinet Shines Bright in the Cybersecurity Universe

Riding secular tailwinds with profitability and scale

Cybersecurity spending continues to accelerate, with global outlays above $211B in 2025, up 15% from the $184B in 2024. It should reach more than $420B in 2030, representing a 13% to 15% CAGR. As companies modernize their infrastructure and threats grow more sophisticated, demand for integrated, scalable security solutions remains strong.

In this fast-growing cybersecurity universe, Fortinet (ticker: FTNT) stands out as one of the most compelling companies. It is not only one of the largest pure-play cybersecurity firms, but also one of the few that has consistently maintained strong profitability over the years. In this article, we will take a closer look at Fortinet’s business, evaluate its fair value, dig into key financial metrics, and estimate the potential returns for long-term shareholders. Additionally, we will identify attractive entry points for those considering a position in the stock.

If you are interested in this sector, you can read my article about it!

I also wrote an article about Palo Alto Networks that you can find just here.

The business model

Fortinet’s business model, as illustrated in the image, is built around providing a comprehensive cybersecurity platform that integrates three core pillars: Secure Networking, Unified SASE, and Security Operations.

Secure networking

Fortinet’s foundational offering lies in Secure Networking, which combines high-performance networking with integrated security. This segment includes:

Network Firewall. Fortinet's flagship FortiGate firewalls are widely deployed to protect network perimeters

Wireless and Wired LAN. Secure LAN offerings for enterprise connectivity

5G. Security for next-gen mobile networks

OT Security. Solutions for operational technology (industrial control systems)

NAC (Network Access Control). Managing and securing devices connecting to the network

Security operations

Fortinet supports Security Operations Centers (SOC) with a suite of tools that enhance visibility, automation, and response:

SOC Platform. Core infrastructure for monitoring and response

Endpoint Protection. FortiEDR and FortiXDR for device-level defense

Network Detection & Response (NDR). Identifies threats across the network

Data Protection, Identity. Enforces data privacy and identity controls

Exposure Assessment. Proactively identifies vulnerabilities and attack surfaces

This positions Fortinet in the growing XDR (Extended Detection and Response) space, enabling enterprise-wide threat management across endpoints, networks, and clouds.

Unified SASE

Fortinet is expanding aggressively into SASE (Secure Access Service Edge), targeting the growing demand for cloud-delivered security and networking for distributed workforces. This pillar includes:

SD-WAN. Securely connects branch offices and remote sites

SSE (Security Service Edge). Core cloud-delivered security services

Single-Vendor SASE. Fortinet provides both networking and security natively

ZTNA (Zero Trust Network Access). Secures remote access to applications

DEM (Digital Experience Monitoring). Ensures quality and performance of applications

Cloud Firewall, WAF (Web App Firewall), CNAPP (Cloud-Native App Protection Platform). Cloud-specific protections

As enterprises move to hybrid work and cloud environments, Unified SASE enables Fortinet to be a one-stop shop for secure connectivity, replacing multiple point products.

Product vs service

Fortinet generates revenue primarily from two categories:

Product revenue. Hardware and software sales (e.g., FortiGate firewalls, switches, wireless access points)

Service revenue. Recurring revenue from security subscriptions and technical support (e.g., FortiGuard security services, FortiCare support, cloud offerings)

Product revenue accounts for approximately 1/3 of total sales, while service revenue makes up the remaining 2/3. In 2024, service revenue grew faster than product revenue (20% vs 12% YoY). Notably, the primary growth driver was Fortinet’s SASE offering, which delivered 28% YoY growth in annual recurring revenue (ARR).

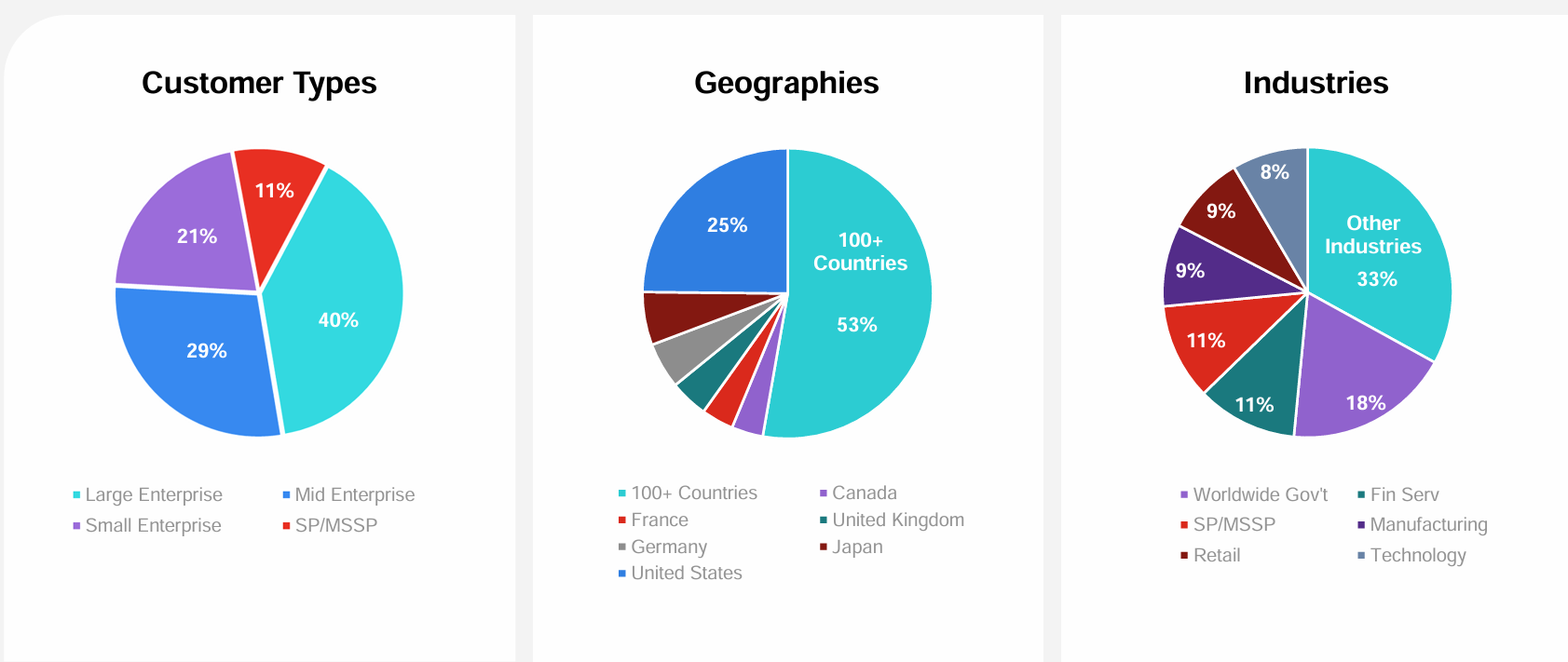

Revenue diversification

The company is highly diversified (company size, geographies and industries) with the US representing only 25% of the sales.

Strategy of the company

There are two key strategic elements that set Fortinet apart from other cybersecurity companies.

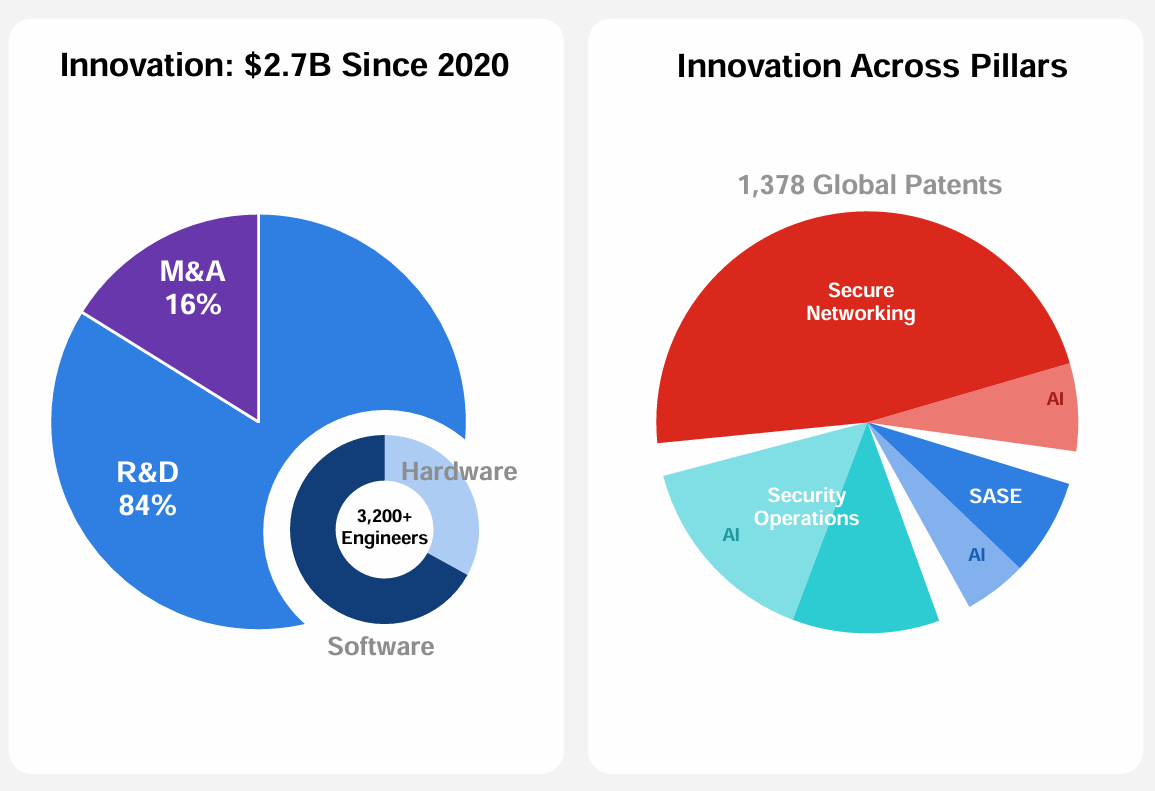

First, Fortinet relies heavily on its own internal R&D rather than aggressive mergers and acquisitions. This contrasts with peers like Palo Alto Networks, which have pursued growth through frequent M&A to expand their product portfolio.

Second, Fortinet’s capital allocation strategy is notably more shareholder-friendly. While many cybersecurity firms are criticized for excessive stock-based compensation (SBC) and shareholder dilution, Fortinet maintains a disciplined approach. Its SBC levels are relatively modest (compared to others at least), and the company actively engages in share buybacks, which support earnings per share growth and enhance shareholder value ($6.4B share buyback programs in the last decade).

Lastly, Fortinet stands out for its consistent focus on profitable growth. Unlike many high-growth cybersecurity peers that prioritize expansion at the expense of profitability, Fortinet has maintained solid margins while scaling.

Naturally, AI and the wide range of opportunities it brings are a key focus for the company and are expected to be a major growth driver moving forward.

Outlook

The company estimates that its Total Addressable Market (TAM) will grow at a 12% CAGR through 2028, and it expects to outpace the market slightly, continuing to gain share across its core segments.

Fortinet operates across three primary business areas:

Secure Networking is projected to grow at around 7% annually, making it the slowest-growing segment and gradually becoming a smaller portion of the overall business

Unified SASE is expected to grow at a robust 18% CAGR, serving as the main growth engine, fueled by cloud adoption and hybrid work trends

Security Operations is forecasted to grow in line with the broader market at approximately 12% per year. However, this area is expected to be heavily impacted by AI, which will enable new product offerings and should drive margin expansion through operational efficiencies

As of the end of 2024, Fortinet holds a net cash position of around $2B, which it primarily plans to use for share repurchases, supported by a current $2B buyback authorization. While Fortinet continues to generate strong free cash flow, which could support acquisitions in 2025, its M&A strategy remains conservative. The company typically acquires smaller firms (3 in 2024, for example) to enhance its platform capabilities. That said, pursuing larger acquisitions could potentially accelerate growth if aligned with strategic priorities.

The rest of this article (including risks, opportunities, fair value analysis, buying zones, and key metrics) is available exclusively to paid subscribers.

By joining as a paid subscriber, you will unlock my most valuable insights, gain full access to my portfolios and real-time moves, and use custom stock screeners to discover new ideas. It is a great way to learn, sharpen your investing mindset, and find high-quality stocks to become a better investor.

Keep reading with a 7-day free trial

Subscribe to Quality Stocks to keep reading this post and get 7 days of free access to the full post archives.