In the world of ETFs, the TOLL ETF (Tema Monopolies and Oligolies) stands out for its focus on investing in companies with a strong competitive advantage. This article will provide an in-depth overview of the ETF, including its performance, top holdings, and an analysis of its investment strategy.

Please note, this is neither a sponsored article nor investment advice. The TOLL ETF is discussed here because its approach offers valuable insights into the philosophy of quality investing. The ETF manager's focus on companies with durable moats aligns closely with long-term quality investing principles, providing valuable insights for investors.

An active ETF

Unlike most ETFs that passively track an index, TOLL is an active ETF. But what exactly is an active ETF, and how does it differ from a mutual fund?

An active ETF is a fund where a manager actively selects and adjusts the portfolio to outperform a benchmark or achieve specific goals, unlike passive ETFs that simply track an index. Active ETFs trade on exchanges throughout the day, providing real-time pricing and liquidity, which sets them apart from mutual funds that only trade at the end of the day at the Net Asset Value (NAV).

Active ETFs tend to have lower costs than mutual funds but are generally more expensive than passive ETFs due to management fees.

In terms of transparency, most active ETFs disclose their holdings daily, whereas mutual funds report quarterly. Overall, active ETFs offer the flexibility and tax benefits of ETFs combined with the strategy of active management, making them a middle ground for investors seeking active strategies with lower fees and more flexibility than mutual funds.

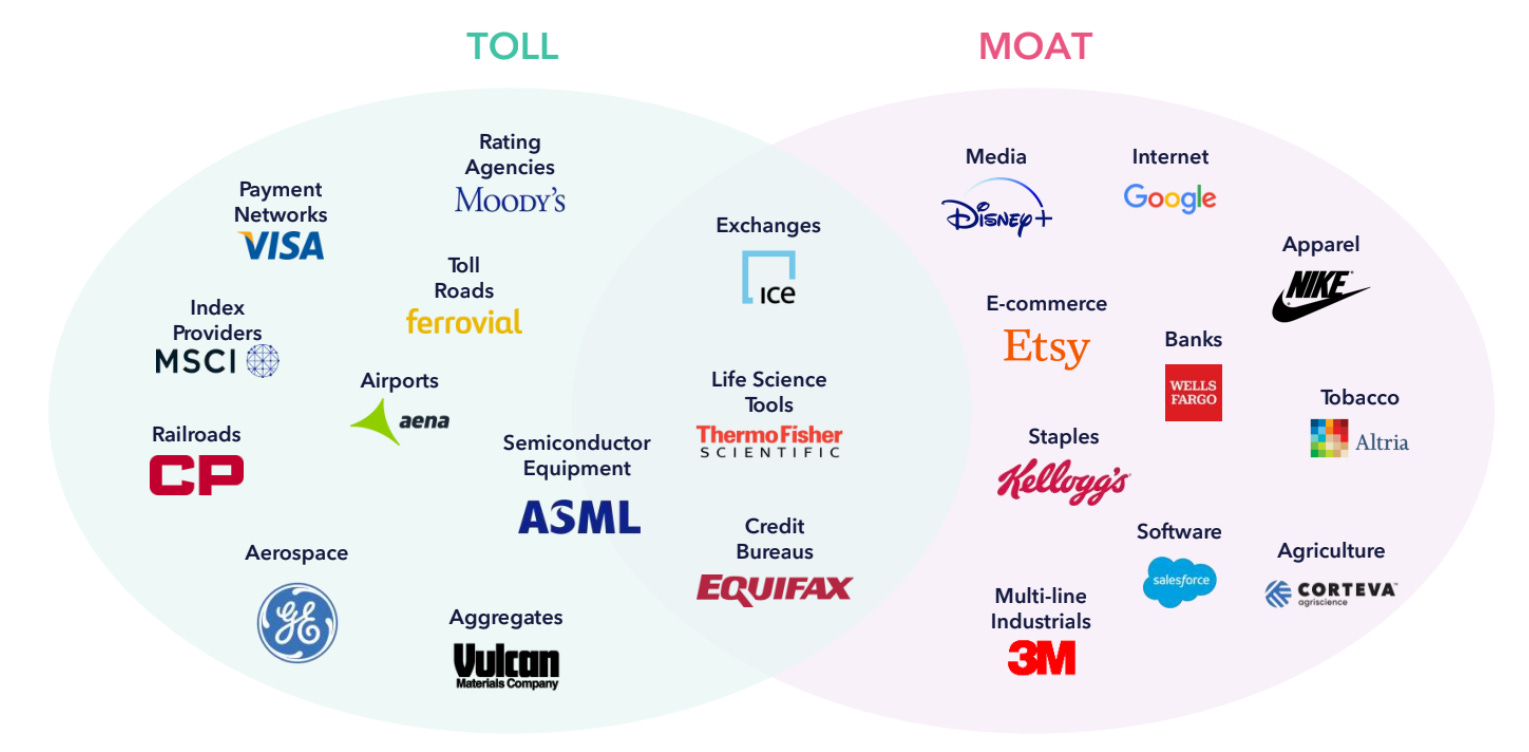

Wide moat vs durable moat

As I describe in this article about moats, the common definition of moat has 5 sources:

Network effect

Intangible assets

Cost advantage

Switching costs

Efficient scale

In the ETF moat approach, the moat has to be durable, tangible and dominant. Intangible assets (primarily brand strength) and sources of cost advantages are substituted with regulation and irreplaceable physical assets.

The underlying premise is that some moats are less tangible and therefore more vulnerable. A brand, for instance, can diminish if consumer preferences shift. In contrast, non-replicable physical assets, exclusive intellectual property (such as patents), and regulated monopolies offer stronger, more enduring competitive advantages.

Consequently, the TOLL durable moat strategy focuses on sectors such as toll roads, railroads, airports, payment networks, rating agencies, semiconductor equipment, and exchanges. As a result, brands and highly competitive B2C sectors are intentionally excluded from this approach.

In terms of stock return, moat firms generate on average higher returns on invested capital (above 15-17% consistently). Returns have the potential to compound significantly over time.

The current stocks in the ETF

The ETF holds 27 companies. Below is the list of these companies along with the reasons for their competitive advantages:

Moody's. Strong regulation and switching costs as its credit ratings are embedded into regulatory frameworks and investor processes.

GE Aerospace. Irreplaceable physical assets and switching costs due to its advanced engine technologies and long-term aircraft contracts.

Intercontinental Exchange. Network effect and regulation from its role in global exchanges and financial markets, with deep liquidity pools.

Visa. Powerful network effect from its global payment network connecting billions of consumers and merchants.

S&P Global. Regulation and switching costs, as its ratings and data services are crucial to regulatory compliance and investor decisions.

Fair Isaac. Switching costs due to its credit scoring algorithms being deeply embedded in financial systems.

Sherwin-Williams. Switching costs and efficient scale, as its wide distribution network and brand loyalty create high barriers for competitors.

Tyler Technologies. Switching costs, providing software solutions to government entities with deeply integrated systems.

Teradyne. Irreplaceable physical assets in testing equipment, with specialized technology difficult to replicate.

Equifax. Regulation and switching costs due to its central role in credit reporting and consumer data systems.

KLA Corporation. Irreplaceable physical assets and efficient scale from its critical role in semiconductor manufacturing inspection.

MSCI. Switching costs and network effect due to its essential indices and data services for global investment portfolios.

Intuit. Switching costs through its widely used tax and accounting software, which integrates deeply into customer habits.

Copart. Efficient scale and network effect in the online auctioning of salvaged vehicles, with a vast network of buyers and sellers.

Vulcan Materials. Irreplaceable physical assets and efficient scale due to its dominant position in aggregate materials essential for construction.

CME Group. Network effect and regulation, with massive liquidity pools and regulatory oversight in financial derivatives markets.

Thermo Fisher. Switching costs and efficient scale, providing specialized lab equipment and services that are difficult to replace.

ASML. Irreplaceable physical assets and efficient scale due to its monopoly-like position in EUV lithography machines used in semiconductor manufacturing.

Canadian National Railway. Irreplaceable physical assets and efficient scale due to its vast rail network covering key North American trade routes.

Aon. Switching costs and efficient scale in risk management and insurance brokerage, with deep client integration and global reach.

Waters. Switching costs with its specialized lab and testing equipment deeply embedded in customer operations.

Texas Instruments. Efficient scale and irreplaceable physical assets with a dominant position in analog and embedded semiconductors.

Bio-Techne. Switching costs from its high-quality reagents and research products that are critical for biotech research and difficult to substitute.

Otis. Switching costs and efficient scale from its global elevator and escalator service network, with long-term service contracts.

Merck & Co. Regulation and irreplaceable physical assets due to its proprietary drugs and strong patent protection in the pharmaceutical industry.

Airbus. Irreplaceable physical assets and efficient scale due to its massive aerospace manufacturing capabilities and long-term aircraft contracts.

It is worth noting that none of the Magnificent 7 stocks are included in the ETF. This is a deliberate choice by the ETF manager to reduce exposure to these heavily represented companies. However, this could be seen as a potential risk, as outperforming the S&P 500 may be challenging without any of these high-performing stocks.

Performance

The ETF is quite new. The performance is +18% YTD - under the S&P 500 but decent considering that there are no Magnificent 7 in the ETF. Currently, the ETF is too new to provide sufficient historical data for a comprehensive performance analysis.

Conclusion

Given that the ETF is relatively new, its historical performance is not yet meaningful. However, it will be interesting to track its future performance against major benchmarks like the MOAT ETF, MSCI World, and S&P 500. This will help assess whether the ETF's approach of selecting companies based on its distinct definition of competitive advantage can outperform the more traditional moat strategies.

ASML's monopoly on EUV tech is fascinating.