Uber, a Business Model in Danger or an Undervalued Fast Grower?

Diving into the secrets of one of the most famous apps in the world

Uber is a very famous app and even gave its name to the word “uberization”, which refers to the act of changing the market for a service by introducing a different way of buying or using it, especially through mobile technology. The stock is actually one of my 12 picks for 2025.

Many investors believe that Uber's current business model is at risk due to autonomous vehicles. Is this true? Could it present an opportunity instead? What does the future hold for the company? Let’s explore these questions in this article!

The business model

The company reports two types of revenue:

Gross revenue refers to the total amount spent by customers on the platform. This includes partner revenue plus Uber's fees.

Net revenue refers to the fees Uber collects. This is the standard way of calculating Uber's revenue.

Uber has three main revenue streams:

Mobility is the original core business. It focuses on its ride-hailing service, connecting passengers with drivers for transportation in cities worldwide. This sector capitalizes on the growing demand for convenient, on-demand transportation.

Delivery is primarily driven by Uber Eats, which connects customers with restaurants for food delivery. Uber Eats has become one of the largest food delivery platforms globally.

Freight provides an on-demand marketplace for shipping freight, connecting truck drivers with shippers who need to transport goods. After strong growth in 2022, this segment has slowed down.

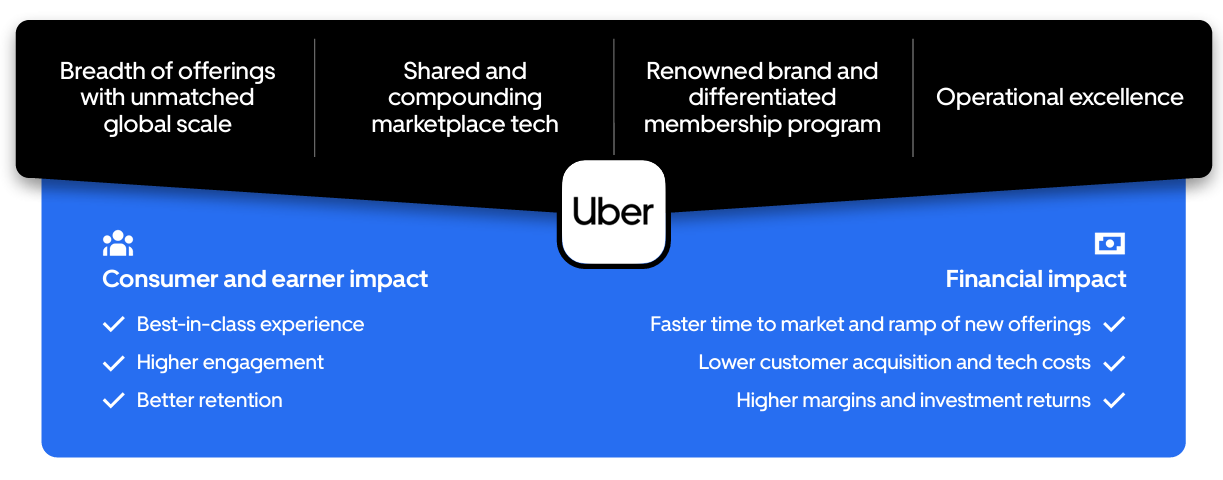

Strength of the platform

Over time, as more users, drivers, and restaurants join the platform, it becomes increasingly valuable. This is the exact definition of the network effect. It also provides a solid foundation for introducing new offerings.

By offering a wide range of services and maintaining a great customer experience, Uber ensures it stays ahead of the competition.

It is noteworthy that customers use more and more different services on the platform. The number of customers using the platform is also growing fast. A multi-product customers consume more than 3x more than a basic customer. This mix in a single platform allows to push customers to the other: 30% of the delivery first trips come from mobility and 22% of the mobility first trips come from the devivery app.

We see the same usage increase for customers subscribing to Uber One. This subscription model increases fidelity of the customers but also improve the business model and create new revenue streams.

A new model focused on profitability

Uber has been profitable since 2023, and the key factor behind this is the increase in the company’s take rate on gross revenues. It has risen from 15% at the start of 2021 to 27% today.

Looking ahead, revenue is expected to grow at a compound annual growth rate (CAGR) of 14% next year, while EBITDA is projected to increase by 30% - 40% annually. This growth will generate significant cash flow, allowing Uber to reinvest in its current operations and explore new opportunities.

Optionalities

What is truly interesting about Uber is its ability to continuously add new revenue streams. We have already seen this with food delivery and subscription services, and now, advertising revenue is also on the rise.

The vast amount of data Uber collects is another key asset, as it can be leveraged and sold. The company has also announced plans to expand into new areas such as enterprise solutions, last-mile logistics, and travel.

Becoming a super app is clearly the direction they are headed.

Autonomous vehicles: risk or opportunity?

Waymo is advancing rapidly and already offers rides in autonomous vehicles. Tesla is also heavily investing in this segment with its Cybercab concept. Investors fear that these companies (or new entrants) could completely disrupt Uber’s business model, which explains the company’s relatively reasonable valuation.

In the worst-case scenario, it would take years for this disruption to occur, giving Uber plenty of time to adapt. However, I don’t believe in the worst-case scenario. The more likely outcome is that companies like Waymo and Tesla will use Uber’s platform in addition to their own systems. Even for them, replicating an ecosystem as strong as Uber’s will be incredibly difficult.

If these companies build their own platforms, they will likely still utilize Uber’s. A similar dynamic can be observed in the hotel industry: while each hotel brand has its own website, most are also listed on Booking.com. The partnership between Waymo and Uber illustrates that, for now, this hybrid model is the one being adopted.

That said, autonomous vehicles remain one of the major risks for Uber. It is up to each investor to decide how significant this risk is.

Before diving into stock metrics, SWOT analysis, fair valuation, buying zones and potential TSR calculations, subscribe now to gain full access to this section. Unlock exclusive access to my content, including in-depth stock analyses, screening tools, industry reports, and valuable portfolio insights!

Keep reading with a 7-day free trial

Subscribe to Quality Stocks to keep reading this post and get 7 days of free access to the full post archives.