Small Caps in 2025 and Beyond: Ready for a Decade of Growth?

Why market cycles may finally favor the forgotten segment

After more than a decade of lagging behind their larger peers, small-cap stocks may finally be entering a period of renewed interest. For years, the small-cap segment has struggled to keep pace with the relentless rise of mega-cap tech giants and defensive blue chips.

But 2025 finds the market at a potential turning point. With monetary policy normalizing, inflation settling (at least expected to settle), and historically low valuations, the small-cap universe could be poised to regain performance. Valuations in many corners of the small-cap market now reflect years of skepticism, offering an intriguing setup for patient investors.

Is this the start of a small-cap renaissance? In this article, we explore the factors that could set the stage for a decade of small-cap outperformance.

Signs of a new cycle

These 2 charts provide strong historical context for the thesis that small caps may be due for a comeback, but they also highlight why timing and patience are critical.

The first chart shows clear cycles of relative performance between small caps and large caps, with multi-year stretches of outperformance alternating with long periods of underperformance. Notably, the recent 14-year stretch of large-cap dominance (2011–2024) mirrors past large-cap cycles in both duration and slope. Historically, such long stretches have tended to reverse, often leading to a decade or more of small-cap outperformance. This cyclical behavior supports the idea that markets may now be primed for another shift back toward small caps.

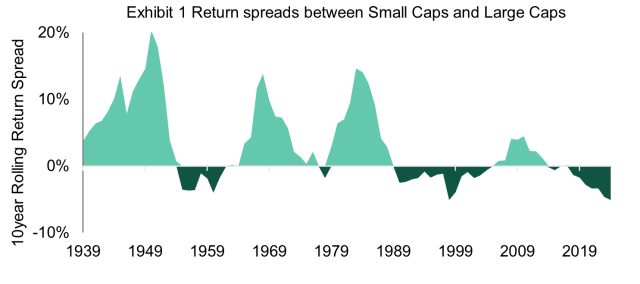

The second chart (the 10-year rolling return spread) further illustrates this cyclicality, showing how small-cap leadership tends to swing in long arcs. What stands out is the depth and persistence of the negative spread over the last decade, one of the longest and most pronounced periods of large-cap dominance since the 1980s. If history is any guide, these extremes have often been followed by strong reversals.

Of course, these patterns are not guarantees, anything can happen. It is important to stay cautious and view them as indicators of increasing probability, not certainty.

Fundamental drivers of potential outperformance

Several factors suggest that small-cap stocks could be poised for a period of outperformance, not just as a rebound from recent weakness, but as a structural opportunity. While past cycles do not guarantee future results, the following dynamics create a compelling case for renewed investor interest in small caps:

Faster growth potential. Small-cap companies, by nature, tend to have greater room for expansion than mature large-cap firms. They often operate in niche markets, emerging industries, or are early in their growth cycle. In a world where economic growth is expected to normalize rather than accelerate, companies with internal growth drivers may attract renewed investor focus

More attractive valuations. After a prolonged period of underperformance, small-caps now trade at historically low valuation multiples relative to large caps. PEs in many small-cap indices reflect years of investor skepticism. Historically, investing at times of low relative valuations has delivered superior long-term returns

Rising M&A activity. Periods of small-cap underperformance often precede waves of mergers and acquisitions. Larger companies and private equity funds look for undervalued, high-potential targets and the current valuation gap makes small caps an attractive hunting ground. An uptick in M&A can provide direct upside for investors holding takeover candidates (as for Cantaloupe or Altium in my small-cap portfolio!)

Potential shift in market flows. Over the past decade, passive flows and mega-cap concentration have fueled large-cap dominance. However, signs of rotation toward active management, equal-weight strategies, and style diversification could redirect flows into smaller names. As investor preferences evolve, small-cap stocks may capture a larger share of capital, providing a secondary catalyst for performance

Of course, there are other potential factors (value versus growth dynamic, inflation and interest rates, deglobalization, or infrastructure investments) but I find these arguments less compelling and harder to translate into a strong investment thesis.

Conclusion

As you know, my small-cap portfolio has delivered strong returns: over 50% in just 18 months. This performance reflects a disciplined and selective stock-picking process, prudent risk management, and, importantly, the renewed flow of capital and investor interest into small caps. If we are indeed at the start of a new cycle, this outperformance could have room to run.

If you are curious, feel free to take a look at my small-cap portfolio!