A look at the growth chart of ServiceNow since 2010 is enough to understand the magic behind the company. Not only do they manage to add new customer but they also expand the revenue of the existing ones.

The stock performance did follow these results. 3y performance +40% / 5y performance +162% / 10y performance +1,139%.

In this article, we will describe the company, its business model and its activities. We will then look at the outlooks and risks the company is facing. At the end, we will review the metrics of the company and evaluate the fair value of the stock.

Company overview

ServiceNow offers a platform to manage digital workflows for entreprise operations. The Now Platform optimizes processes, connects and unifies data to use them easily. It is divided into 4 segments:

Technology workflows. Here you find different modules about IT service and systems management.

Employee workflows. HR service, legal system and workplace service delivery.

Customer and industry workflows. Customer service, field service and industry management.

Creator and FSC (Finance and Supply Chain) workflows. Here you can find a lot of different modules from procurement to automation engine.

The platform continuously evolves and new modules are added. For instance, for 2024 the roadmap includes 3 new modules: digital end-user experience, contract lifecycle management and sales and order management.

The company targets several key industries with significant growth potential: retail, public sector, manufacturing, financial services, healthcare & lifesciences, telecom, media & technology.

The core customers of the platform are CIO (Chief Information Officer). This is a smart entrance as those ExCom members have access to budgets and CAPEX. By developping new features, Servicenow also wants to discuss directly with other departements (human resources, logistics, supply chain, finance, operation, security, business).

The performance of the company is staggering. Number of customers above $20M revenue has been multiplied by 2.2x from 2021 to 2023. The renewal rate is above 98% and 70% of customers grew their spendings on the platform in 2023.

Growth drivers

The strategy of the company is focused on the innovation for its platform. They search to increase their TAM (Total Addressable Market) through product innovation, horizontal development and new industries penetration. The always wider functional coverage allows the company to leverage the data present on the platform and the architecture.

The primary customers are CIO. This extension of functionalities also allows the company to help the CIO to reduce the number of applications in their architecture - another argument to use new modules.

The result is the TAM expansion from $39B in 2015 to $275B expected in 2026. The breakdown inside the $275B is:

$108B for Technology Workflows

$15B for Employee Workflows

$68B for Customer and Industry Workflows

$84B for Creator and FSC Workflows

AI is also a strong growth driver. It will allow the company to offer more service to its customer and the wide functional coverage of its products will allow to have better use case than its competitors. The potential revenues due to AI are expected around $3.5B (30% of the current sales)

They also want to expand internationally using a strong partner network for distribution and implementation. 6 markets have been identified to have the potential to go above $1B revenue: UK, Germany, Canada, France, Japan & Australia. Other markets, less mature, also have a huge potential like India or Brazil.

Stock-based compensation

As always for this kind of companies (great quality, incredible growth - Crowdstrike, Palo Alto, etc), SBC is an issue.

Let’s analyze some metrics for Servicenow:

2021 - $1.131B SBC vs $1.867B FCF

2022 - $1.401B SBC vs $2.180B FCF

2023 - $1.604B SBC vs $2.728B FCF

The company wants to reduce its SBC around 10% of the revenue. With a FCF margin of 30%, 1/3 of the FCF will be dedicated to SBC (around $45k per employee). For now, the result is a significant and unecessary dilution. About the dilution, the company aims to go from 1.5% a year in 2019 to less than 1% from 2023.

The fact that management is aware that this is an issue for shareholder return is already a good sign. More effort could be done though.

Peers recognition

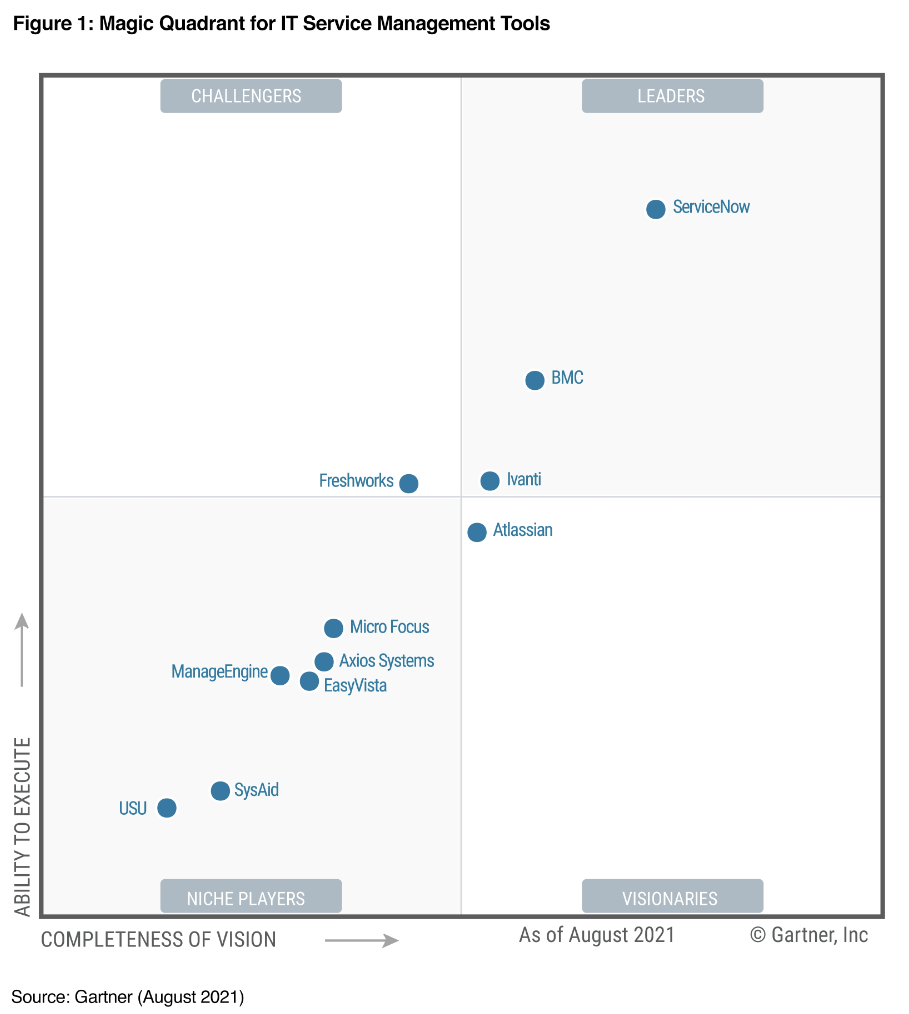

For years, ServiceNow has been named a leader in several categories:

Gartner Magic Quadrant: enterprise low-code application platform, application planning tools

Forrester Wave: third-party risk management (TPRM) platform, digital process automation (DPA) software, customer service solution, value stream management solution, low-code development platform for professional developers

The good peer recognition and the variety of topics is a good illustration of the strategy followed by the company.