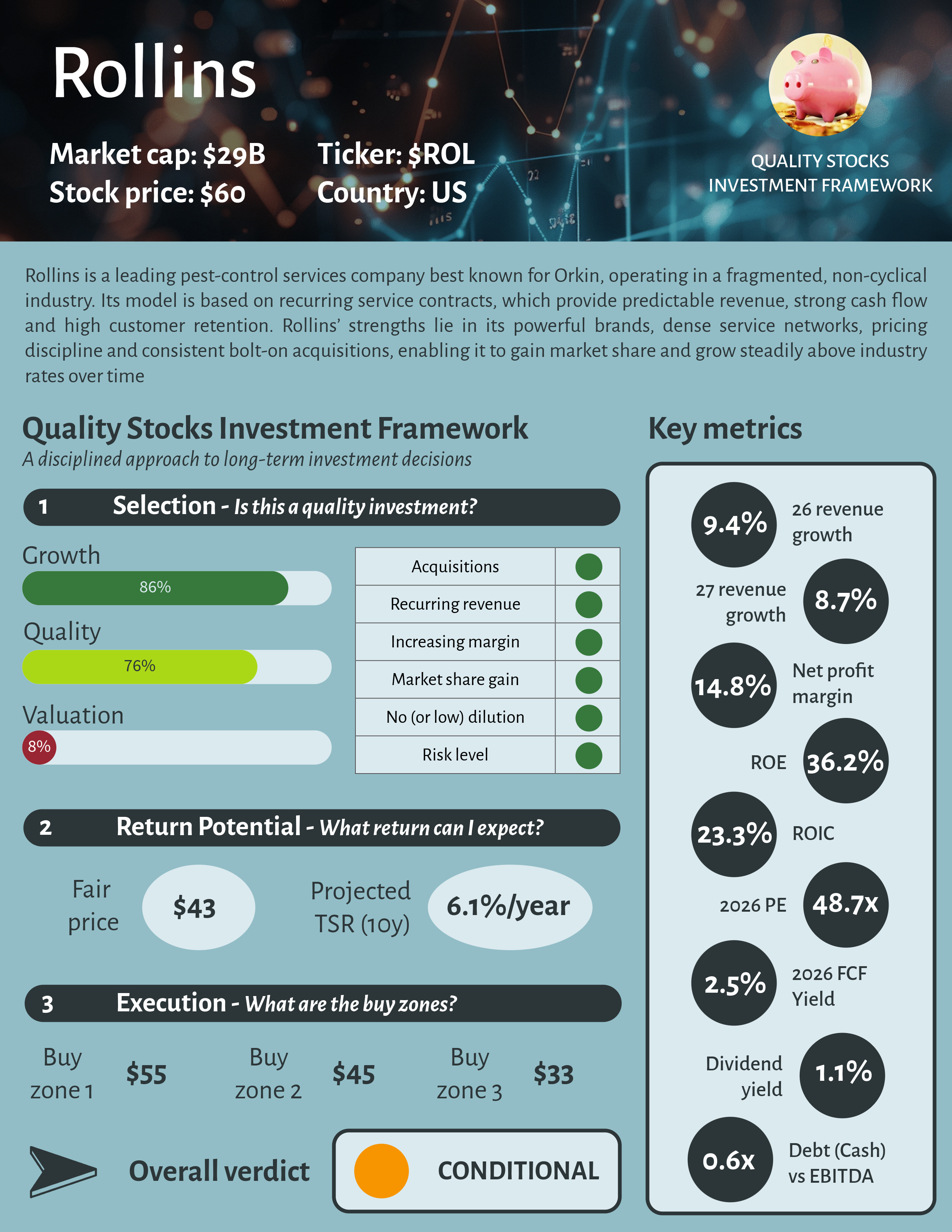

Rollins Stock Analysis: Exceptional Business Quality, Questionable Valuation

Pricing power, recurring contracts and the valuation question investors can’t ignore

Welcome to “Stock Analysis”, a new series where we go beyond headlines to understand how businesses really make money. The series focuses on introducing new investment ideas by highlighting often less-followed companies. Each article applies the Quality Stocks Investment Framework to assess business quality, return potential and identify buy zones, providing readers with the tools and context needed to form their own investment decisions.

For paid subscribers, each Stock Analysis goes a step further by opening up the full reasoning behind the investment thesis and decision process:

Detailed TSR calculations, including all underlying assumptions. This allows investors to understand what must go right for the investment to deliver acceptable returns and to stress-test their own expectations against explicit inputs

Explicit bull and bear cases. It helps frame both upside potential and downside risks, making uncertainties visible rather than implicit and supporting more balanced, risk-aware decisions

My analysis beyond the overall verdict. This provides a deeper insight, enabling investors to form an independent view rather than relying solely on a conclusion

For this 2nd episode, we turn to Rollins, a US-based services company and a global leader in pest control and termite management solutions for residential and commercial customers.

One Pager

The stock at a glance

The business model

Rollins’ business model is based on recurring, contract-driven pest control services, primarily delivered through its flagship Orkin brand. The company provides ongoing residential and commercial pest management through regularly scheduled service plans, which generate predictable revenue, high customer retention and stable cash flows.

Recurring revenue is a key driver of Rollins’ success because it provides predictable cash flows, high customer retention and operational efficiency. Ongoing service contracts ensure regular customer interactions, reduce churn and lower customer acquisition costs, while allowing Rollins to optimize technician routes and pricing over time. This stability enables consistent reinvestment (M&A, technology, marketing, …), reinforcing market share gains and creating a resilient growing business model largely insulated from economic cycles.

The second key driver of Rollins’ success is its disciplined and repeatable M&A strategy. Operating in a highly fragmented industry, Rollins regularly acquires small, local pest-control operators and integrates them onto its national platform, benefiting from brand strength, purchasing power and operational efficiency. These acquisitions are typically low risk, quickly accretive and reinforce local density, allowing Rollins to steadily expand its footprint, gain market share and compound growth without relying on large, transformational deals. A great element for a serial-acquirer.

Last earnings report

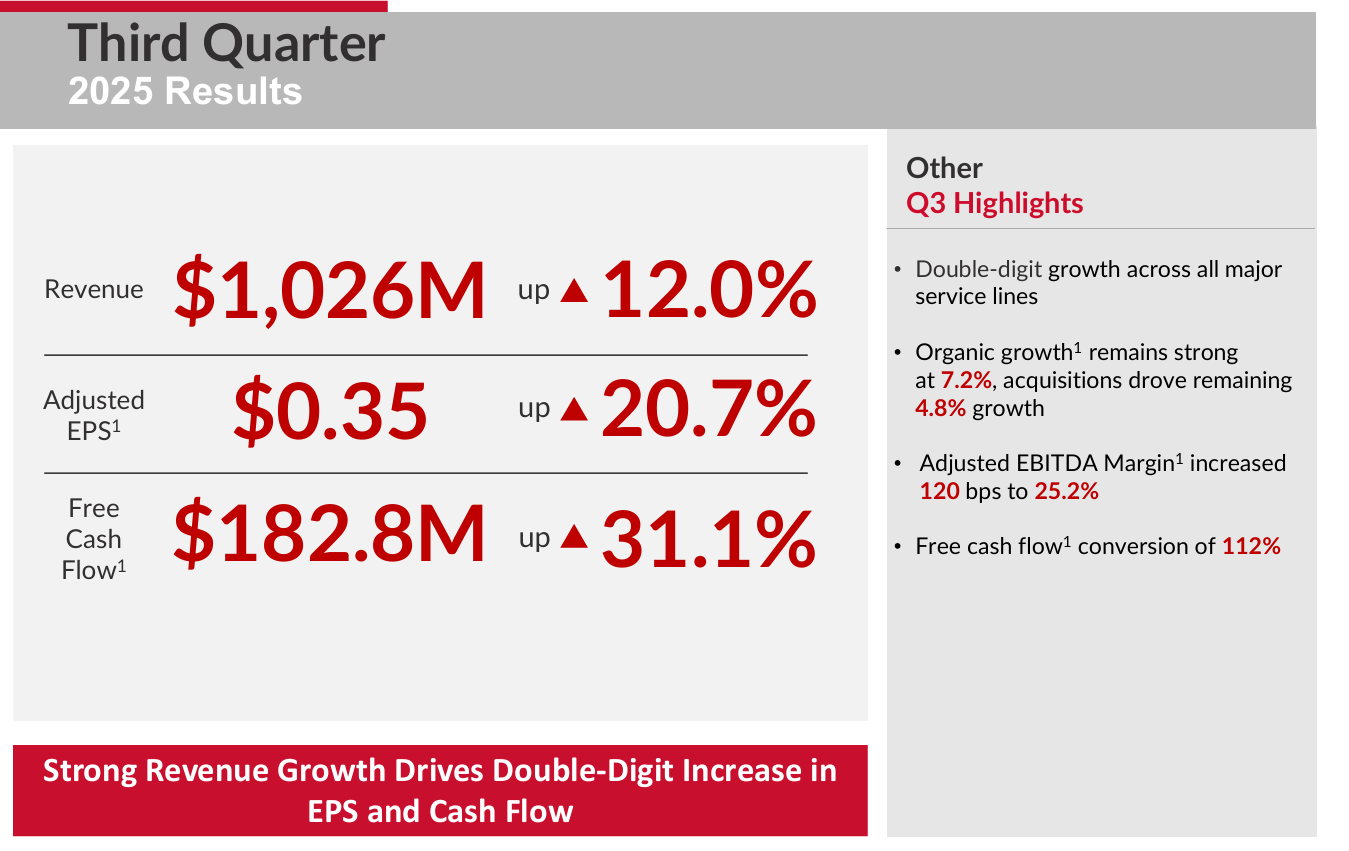

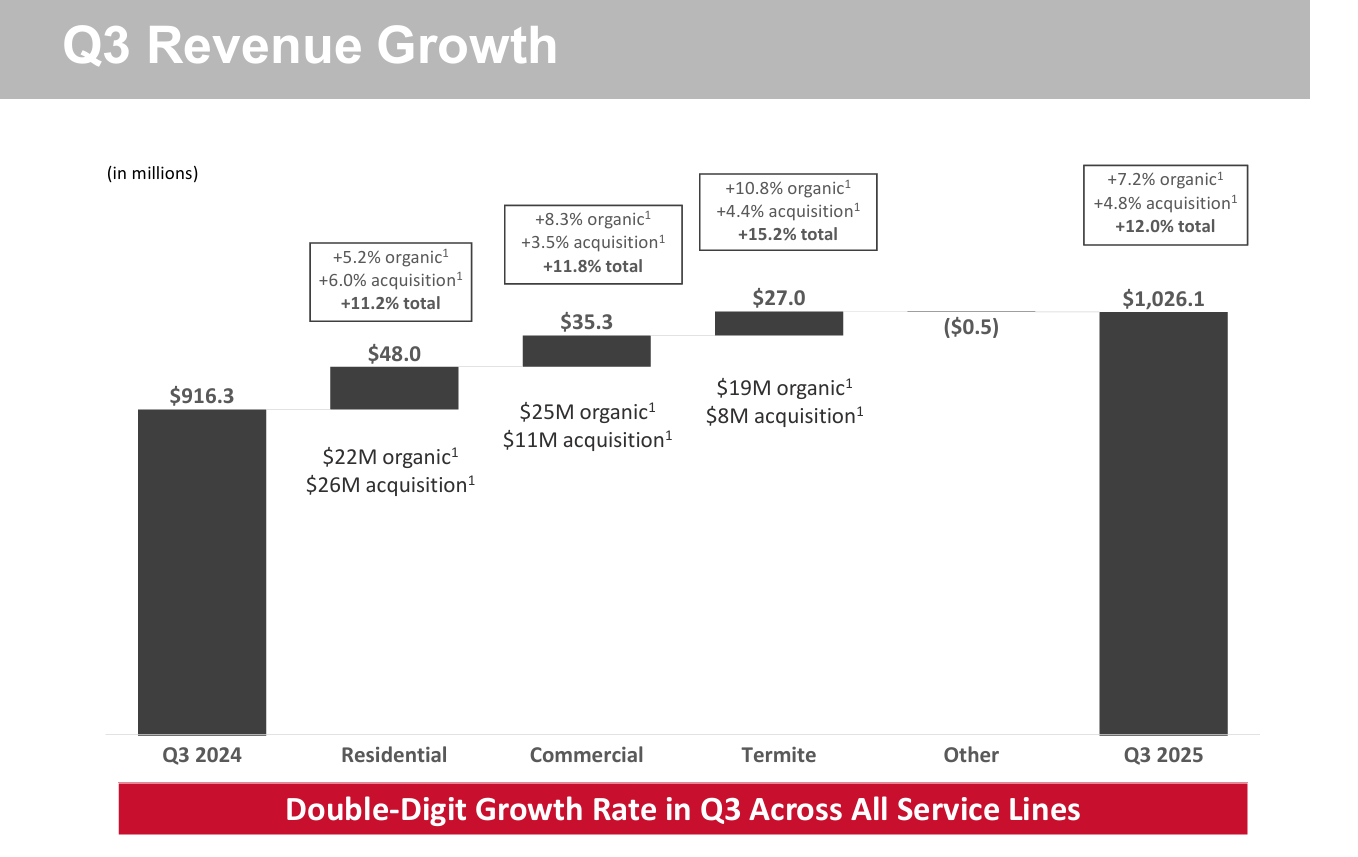

The company earned $1.03B in revenue in its Q3 25, which was 12% higher than the same quarter last year. Organic growth accounted for 7.2% of that increase while the rest came from acquisitions.

EPS were $0.34 (on a GAAP basis), up 21% YoY . Cash flow from operations increased 30% to $191M. All three main business segments performed well

Residential pest control revenue grew 11.2%

Commercial pest control rose 11.8%

Termite and ancillary services increased 15.2%

Margins also improved, with the adjusted EBITDA margin rising to 25.2% (+120bps vs previous year). Management noted strong demand and successful integration of acquisitions.

To go beyond the initial analysis, paid subscribers unlock the detailed TSR calculation with underlying assumptions, explicit bull and bear cases and my full analysis beyond the verdict, providing deeper insight into risks, opportunities and the investment decision process