Paypal, a Payments Giant with Feet of Clay?

Future Outlook: Can PayPal Overcome Challenges and Sustain Growth?

With an ATH of over $300 in 2021, Paypal is known for its rocky stock market history. The current share price is $61, almost 80% lower. However, the payments giant still has qualities and that will be necessary for the challenges that lie ahead. Technological challenges, competition, will the stock manage to return to its former heights? Will management be able to restore investor confidence?

In this article, we will explore the world of Paypal and follow the structure below:

Company presentation (activities, value proposition, global KPIs)

Market overview and projection to 2030

Stock metrics

SWOT analysis to identify the main risks and opportunities

Fair price estimation

Company presentation

The paypal business is divided into the following categories:

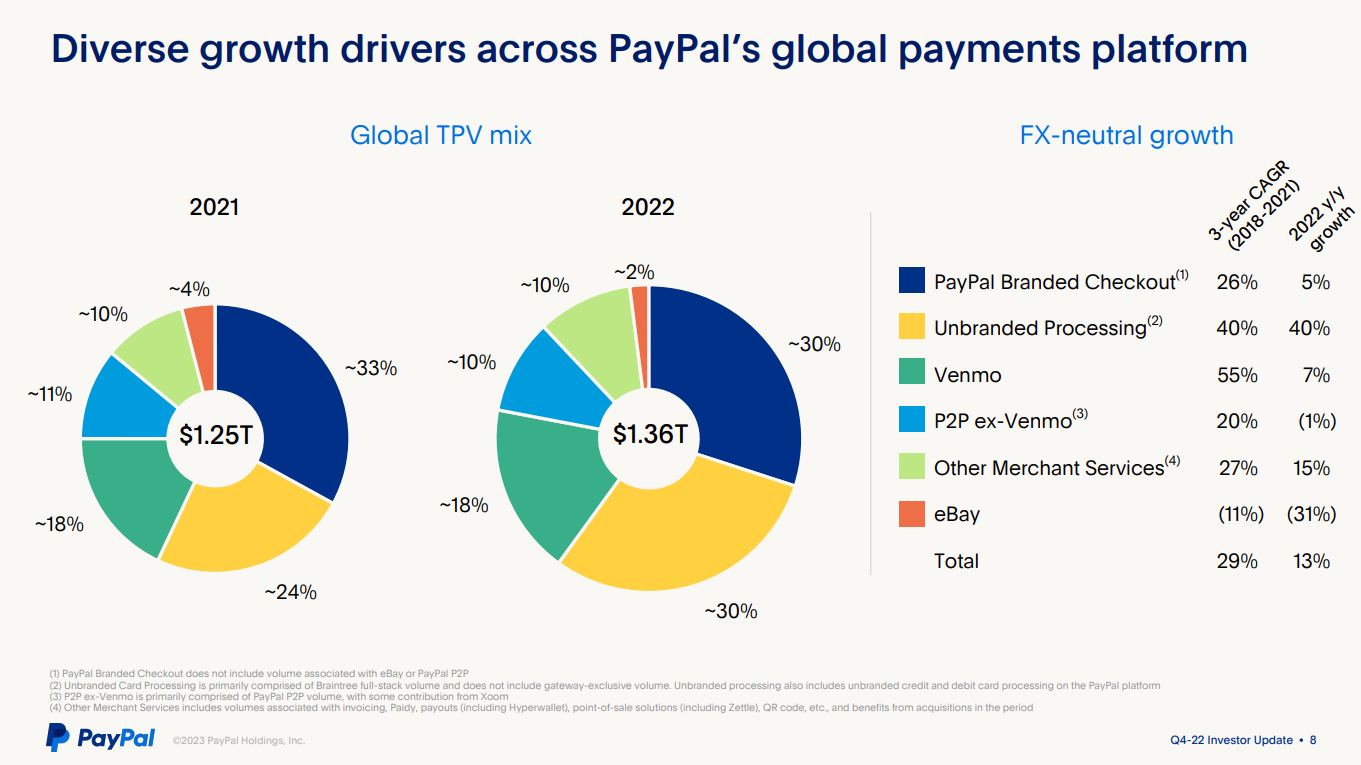

Paypal Branded Checkout for 30% of revenue. It is the core and historical business activity

Unbranded Processing, also for 30% of revenue. It is mainly Braintree, the unbranded payment activity

Venmo for 18% of revenue. It is a mobile payment service, mainly designed for sharing payments with friends and family

The 22% remaining are mainly P2P Ex-Venmo and Other Merchant Services (Point-of-sale solutions, QR code, invoicing)

One thing is immediately clear from the infographic: growth is slowing. For 2022, core business growth (Paypal Branded Checkout) is 5% compared with a CAGR of 26% over the 2018-2021 period. Venmo goes from a CAGR of 55% to 7% growth in 2022. The rest of the P2P business is even declining.

It is not the same story at all. Therefore it is easy to understand the massive drop in valuation. We are not telling a story of 20% annual growth, but a story of 5%. The share price must naturally adjust.

Fortunately, the unbranded payments business continues to enjoy strong growth. The only downside is that margins are lower than for other activities. It is therefore difficult for the market to fully appreciate the growth story behind this activity.

Net profit margin is paypal's second biggest problem. The 2018-2021 average was 15.8%. The expected average for 2022-2025 is 12.5%. Once again, we find one of the reasons for investors' disenchantment with paypal.

The company is nonetheless very appealing. First of all, its value proposition as an intermediary between merchants and buyers is based on facilitating the experience. It is a win-win relationship for all parties.

Some metrics are also quite satisfying. While the number of users tends to stabilize, the number of transactions per user increases significantly, a sign of competitive advantage and user loyalty.

Their market shares are also less likely to shrink than is regularly reported. While growing competition will make it difficult to retain market share at this level for much longer, the situation is likely to be less catastrophic than announced. Only time will tell.

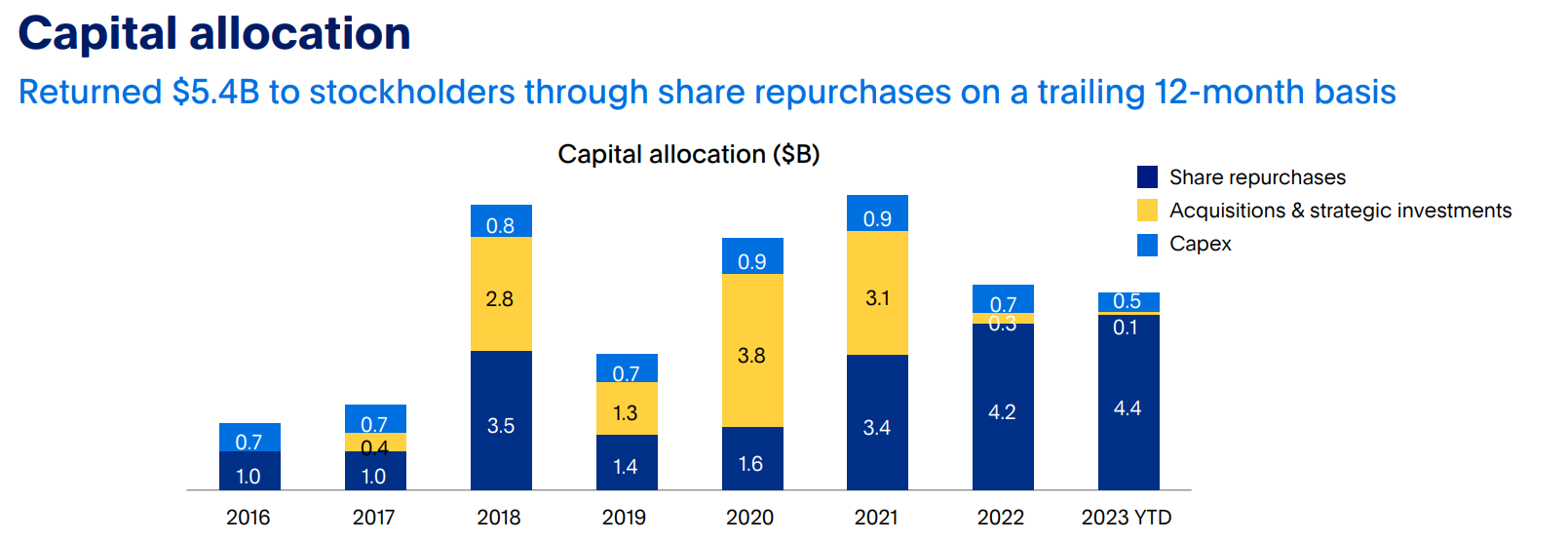

And last but not least, Paypal should be seen for what it is. A mature company, in a buoyant market, with high-growth segments. But above all, a company capable of generating huge FCF. Because, yes, we are dealing with a FCF cow. We will look at this later in the metrics section.

With this FCF, the capital allocation strategy is clear: returning money to shareholders, notably through massive share buybacks. As stock price is cheap at the moment, the effect is particularly visible on the number of shares outstanding.

The payment market

The digital payment market is expected to generate CAGR of between 15% and 20%, according to various studies. This significant growth is nonetheless attracting fierce, high-performance competition.

Numerous segments exist. Here are the most significant companies in this sector: Paypal, Apple, Google, Visa, Mastercard, American Express, Adyen, Worldine, Global Payments, Stripe and Square.

Keep reading with a 7-day free trial

Subscribe to Quality Stocks to keep reading this post and get 7 days of free access to the full post archives.