Is Consulting Dead?

A business model that will dramatically change in the coming years

For a decade, Accenture was the gold standard of the quality compounder: high ROIC, sticky client relationships and a predictable 10–12% annual return. But today, the chart looks more like a distressed tech startup than a blue-chip bellwether. From its peak of nearly $380 in early 2025 (or even above $410 in 2021), ACN has collapsed over 50%, bottoming out near $160. PE went from almost 30x to just above 10x currently.

The market is not just pricing in a bad quarter, it is pricing in an existential crisis. Investors are terrified that the consulting moat is being drained by the very technology (Artificial Intelligence) that these firms were supposed to sell. But is the business model truly broken or is the market failing to see the birth of the new consulting?

What is consulting?

To understand why the stock market has historically treated these firms as quality compounders, one must first understand the fundamental value proposition of the consulting industry. At its core, the business model thrives on 3 pillars: expertise, capacity and neutrality. Clients turn to consultants for expertise when they face a problem they lack the internal skill set to solve, such as navigating a complex cross-border merger or implementing a bleeding-edge technology stack. Beyond knowledge, consulting provides a capacity lever. Large organizations often have the will to change but lack the hands to do it. Consultants act as a variable labor force that can be switched on or off, allowing a company to scale its efforts without the long-term liability of increasing permanent headcount. Finally, the external point of view acts as a form of corporate insurance. A CEO may know exactly what needs to be done, but they hire a consultant to provide a neutral, third-party stamp of approval that can be used to build consensus among a skeptical board of directors or a resistant workforce.

The industry is far from a monolith and the investor must distinguish between the various sub-sectors, each with its own margin profile and moat durability. Strategy consulting sits at the top of the food chain, where firms like McKinsey or BCG command the highest daily rates (above $5k a day). Here, the product is not a finished system but a high-stakes recommendation on where a company should play and how it can win. Just below this is management consulting, which focuses on the how: optimizing operations, restructuring supply chains or managing large-scale organizational changes. These engagements are longer and more integrated than pure strategy, focusing on the bridge between a high-level idea and its day-to-day execution.

The largest and most capital-intensive segment is IT consulting, which is traditionally divided into project and run services. Project consulting involves the design and building of new digital infrastructure, the heavy lifting of installing an ERP system, moving data to the cloud or creating a software from scratch. Once the system is built, the run side of the business takes over, providing long-term managed services and maintenance. This is the recurring revenue that quality investors love, as it creates switching costs for the client. At the very bottom of the hierarchy lies simple body shopping. In this model, the consulting firm essentially acts as a high-end staffing agency, providing bodies to fill seats for basic tasks. This allows the client to bypass the friction of hiring and firing employees while keeping the consulting firm’s bench active.

The current challenges

The core challenge for consulting firms is that AI is not just a tool they sell, it is a force that could fundamentally shrinking the surface area of their traditional business model. The status of these stocks is under siege because the very mechanics that made them profitable (billing for human time) are being liquidated by algorithmic efficiency.

1. The evaporation of junior labor

The traditional consulting pyramid relies on an army of junior associates to handle the grunt work (data cleaning, research and deck formatting). However, recent data from 2026 shows that AI agents now handle approximately 60–70% of these foundational tasks. A landmark study revealed that consultants using AI finished tasks 25% faster with 40% higher quality. For a business model that bills by the hour, this is a deflationary trap. If a junior consultant becomes twice as productive, the firm potentially loses half its billable revenue unless it can double its project volume.

2. The erosion of the expertise moat

Historically, a major moat for large firms was their proprietary knowledge and the speed at which they could train new cohorts. Today, AI allows newcomers and boutique firms to close that gap almost instantly. An entry-level consultant equipped with specialized LLMs can now perform (at least in theory) financial analyses and regulatory cross-referencing that previously required years of experience to master. This commoditization of expertise means that the premium clients used to pay for a big-name firm’s brain trust is being competed away by smaller, leaner AI-native competitors who can deliver the same insights at a fraction of the cost.

3. The empowered executive

The capacity argument for hiring consultants (the need for extra hands to execute a vision) is also weakening. Corporate executives are increasingly using internal AI suites to handle market synthesis and strategic planning themselves. This shift does not just reduce the frequency of consulting engagements, it moves the work in-house, permanently shrinking the Total Addressable Market (TAM) for external capacity.

4. Accelerated implementation timelines

In IT consulting, the setup phase of a project used to be a reliable multi-month (year) revenue generator. New efficient data architectures and automated coding tools have dramatically compressed these timelines. What used to be a multi-year ERP migration or cloud integration is now frequently completed in months (or at least quarters). While this is a win for the client, it is a structural headwind for the consultant. Since stocks are valued on the predictability of long-cycle revenue, the shift toward shorter, high-intensity projects makes earnings more volatile and harder to forecast.

5. The automation of run services

The most defensive part of the business (the run or managed services) is being cannibalized by autonomous monitoring systems. These AI-driven platforms can predict system failures, patch security vulnerabilities and optimize server loads without human intervention. For firms like Infosys or Capgemini, which rely on large-scale maintenance contracts, this automation removes the need for thousands of offshore support roles. Unless these firms can successfully pivot to charging for the software rather than the people managing it, they risk a permanent contraction in their most stable revenue streams.

6. The AI fatigue

By mid-2026, many C-suite executives have entered a phase of AI fatigue. After spending millions on AI pilots in 2024 and 2025, many have found that while the technology is cool, costs and real usage creates lower than expected ROI. However, this investments have reduced the investments in other legacy software, reducing the project dynamic we previously had.

7. The internalization of the digital core

As AI becomes the central nervous system of a business, companies are realizing that they cannot outsource their brain. Large enterprises are increasingly building internal AI orchestration teams rather than hiring external firms to do it for them. This move toward in-sourcing is shrinking the available market for the high-end strategic work that used to be the crown jewel of the consulting world.

Why the market is overreacting

While the market is obsessed with the death of the billable hour, it is likely missing the structural resilience and agility of these consulting giants.

1. The software illusion

The market often conflates consulting with pure labor, forgetting that firms like Accenture and Capgemini have spent the last decade becoming massive software implementation and licensing engines. A significant portion of their revenue is tied to the digital core, managing the underlying cloud architecture and enterprise software (SAP, Salesforce, Oracle) that AI actually runs on (or will run on…). AI will not exist in a vacuum, it requires the very infrastructure these firms are paid to build and maintain. As long as enterprise software remains complex, the plumbing revenue of consulting remains intact.

2. The margin expansion trade-off

Wall Street is currently punishing the sector for slowing revenue growth, but it is ignoring the potential for a massive expansion in productivity. In the old model, growing revenue by 10% required hiring 10% more people, a linear, low-leverage equation. In 2026, if AI allows a firm to deliver the same project with 40% fewer staff, the firm can afford to give the client a 15% discount while still capturing a significantly higher profit margin. We are moving from a volume business to a value business, where the firms will trade top-line vanity for bottom-line sanity (lower revenue, higher margin)

3. The counter-intuitive revenue growth

Despite the efficiency narrative, the aggregate revenue for the industry giants is still hitting record highs. The reason is simple: the complexity gap. While AI makes individual tasks easier, it makes the overall corporate ecosystem much more complicated. This creates a massive, multi-year backlog of work. The market sees AI as a one-off disruption, but for consultants, it is a forever project that requires constant tuning, oversight and integration.

4. The trust premium

In an era where AI can hallucinate and digital security is under constant threat, the value of a brand name consultant has actually increased. A board of directors will not trust a raw LLM to oversee a $500M restructuring. They will trust a firm with a balance sheet, a legal department and a century of reputation.

5. The capital allocation advantage

Finally, the market is missing the sheer fortress nature of these companies’ balance sheets. With stock prices at multi-year lows, firms like Infosys and Accenture are sitting on massive cash reserves. They are in a position to aggressively buy back their own undervalued shares and, more importantly, acquire the very AI startups that are supposed to disrupt them.

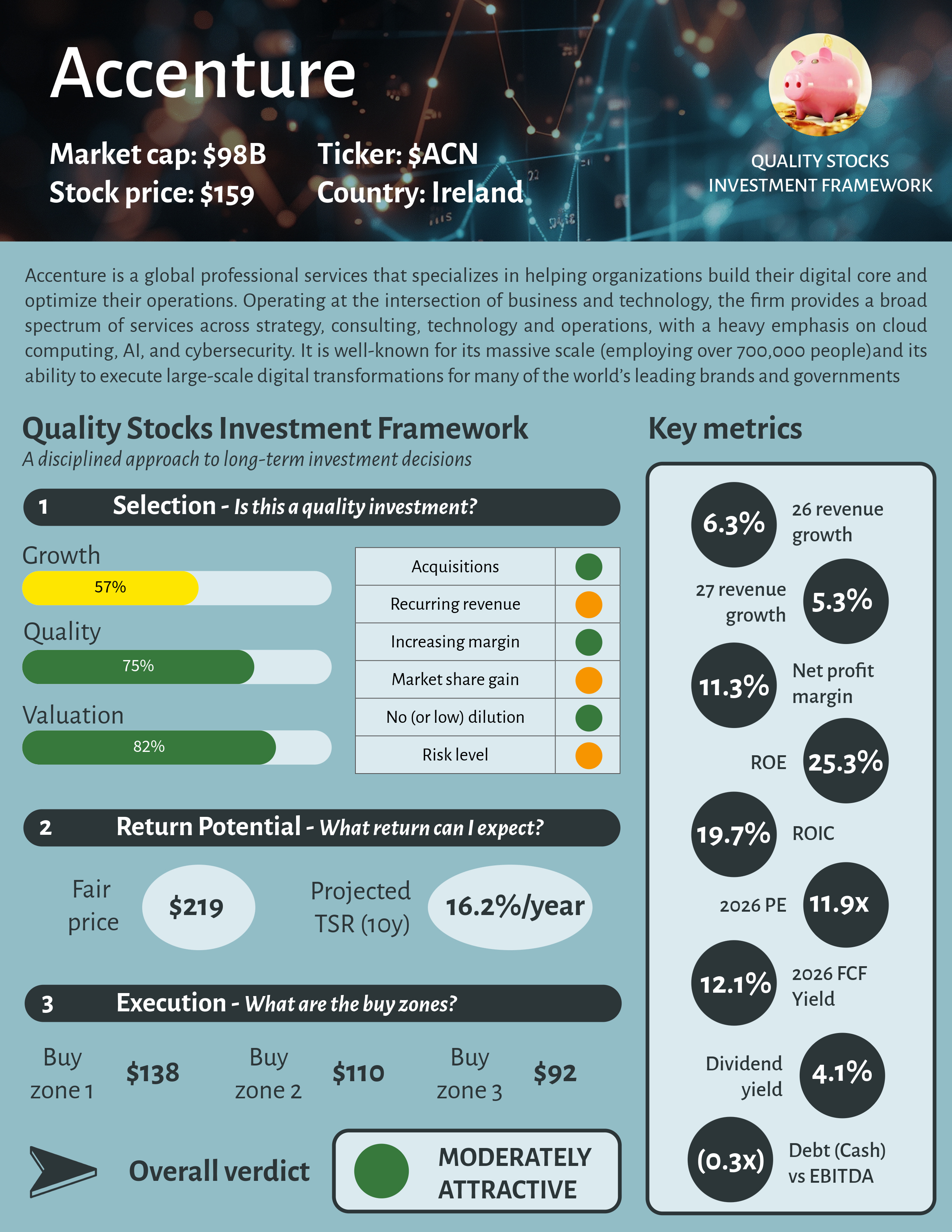

Zoom on Accenture

If you believe the consulting model remains resilient, Accenture’s current valuation represents a compelling entry point. However, the market is currently struggling to price the company accurately due to a volatile mix of macroeconomic uncertainty and shifting industry pressures.

Until the long-term impact of AI is clearly defined (specifically whether it serves as a massive productivity tailwind or a threat to traditional billable hours), the share price may continue to slide. Consequently, it is prudent to avoid going all-in while the market searches for a definitive floor. This setup is not unique to Accenture, as peers like Capgemini, Infosys and Tata Consulting Services face similar headwinds. Nevertheless, the AI revolution will likely favor these larger players who have the scale and capital to integrate the technology most effectively.