How Did Top Luxury Stocks Perform in 2024? A Detailed Comparison

Based on the recently published earnings results

The earnings season is still ongoing, but the top 5 luxury companies have already published their reports. These companies are LVMH, Kering, Hermès, Richemont, and Ferrari. In this article, we will compare their results and outlooks.

If you would like to deepen your knowledge of the sector, I have written two deep dives on LVMH and Hermès.

LVMH

2024 proved to be a challenging year for LVMH, with overall organic growth at just 1% (and a -2% decline on a reported basis due to currency effects). The company's performance showed mixed trends across its business segments:

Wines & Spirits. This segment faced a disastrous year, impacted by tariffs in China and shifting consumer preferences.

Fashion & Leather Goods. Growth was flat and this division represents half of the group’s revenue. A glimmer of positivity came from Q4, which outperformed Q3.

Perfumes & Cosmetics. This segment had a decent year, particularly when compared to certain competitors.

Watches & Jewelry. Although the segment had a difficult year overall, Q4 delivered a positive turnaround.

Selective Retailing. Driven primarily by Sephora, this division continued to perform well, remaining a bright spot for the group.

By region, the results were mixed:

The US and Europe posted modest growth (+2% and +3%, respectively).

Japan saw an impressive 28% increase (now accounting for 9% of total sales, up from 7% in 2023), largely driven by foreign shoppers taking advantage of a weaker yen.

Asia (excluding Japan), primarily China, declined by 11%, making it the key factor behind the company’s overall poor performance.

In 2025, LVMH remains cautious but is focusing on innovation, brand desirability, and creativity to navigate the challenges ahead.

Kering

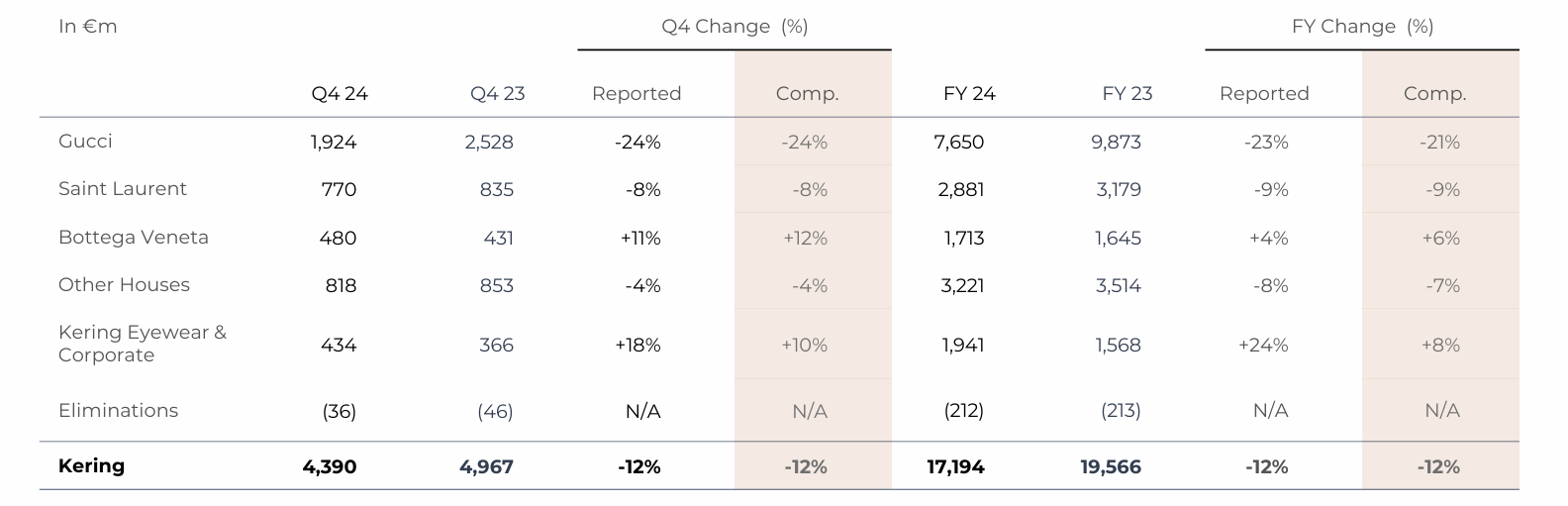

Kering had the worst year among the 5 companies we are analyzing, continuing a trend that has persisted for several years. Performance across its portfolio of brands was uneven, with only Bottega Veneta (+6%) and Kering Eyewear (+8%) delivering positive results. Gucci, which accounts for 45% of the group’s sales, suffered a dramatic decline of over 20% YoY. The one silver lining is that Gucci’s contribution to total sales dropped from over 50% in 2023, reducing reliance on a single brand - probably not for the good reasons.

Asia stood out as the weakest-performing region, further weighing on the group’s overall results.

For 2025, Kering is focused on deleveraging, aiming to reduce its debt from 2.3x EBITDA in 2024 to around 2.0x. To achieve this, the group plans to sell non-core real estate assets.

On the growth front, Kering is prioritizing organic expansion and regaining market share. The company’s strategy includes opening more stores, increasing store density, and strengthening brand desirability to drive consumer engagement and loyalty.

Ferrari

Ferrari achieved 11.8% revenue growth in 2024, with only a modest 0.7% increase in units shipped. The majority of this growth was driven by price increases and a favorable product mix.

Ferrari stands out from its peers by maintaining limited exposure to the Chinese market, a trend that became more pronounced in 2024. China now represents 9% of total sales, down from 11% in 2023.

In 2025, Ferrari plans to launch six new models, with three already unveiled in 2024. The company’s revenue guidance for FY25 targets a 5% growth.

Richemont

Richemont has shifted its fiscal year, so unlike other companies, we will primarily focus on the last quarter’s performance rather than FY24.

The group has seen solid growth, driven primarily by its watches and jewelry divisions, which grew by 10.0%. This segment has performed well across the luxury sector. Notably, jewelry grew by 14%, while fashion and accessories saw an 11% increase. However, watches experienced an 8% decline. Jewelry now accounts for more than 70% of Richemont’s sales, reflecting its dominant role in the product mix.

The only region to report negative performance was APAC, while all other regions showed positive growth.

In terms of sales channels, online retail grew by 17%, underscoring the company’s successful focus on expanding its digital strategy.

Hermès

Among the five companies, Hermès reported the strongest growth in 2024, with a remarkable 13% increase. Even more telling of the company's strength is that all regions posted positive growth, even APAC despite being the slowest-growing region at around 7%. Hermès continues to expand its market share globally.

Growth across Hermès' sectors has been impressive, with leather goods leading the charge at 18%, followed by ready-to-wear at 15% and other sectors at 17%. The only exception was the watches segment, which saw a decline of -4%.

The outlook remains positive, with the company expecting continued growth momentum. Hermès will maintain its focus on its industrially integrated model, with plans to open new factories. Additionally, the group aims to strengthen its supply chain by continuing its acquisitions of key suppliers.

What are your thoughts on the performance of these companies? Feel free to share in the comments!

Comparison

Please note that for Richemont, as mentioned earlier, the reported growth pertains to their Q3 FY25 quarter, not FY24 versus FY23.

Hermès, Ferrari, and Richemont all demonstrated very strong performances. LVMH showed an average performance despite challenging market conditions, while Kering continued to lose market share and posted negative growth. Overall, the trends remain consistent with what we’ve seen in previous quarters.

Interestingly, all five companies have shown positive stock performance so far this year. Their YTD returns are as follows:

+22% for Hermès

+16% for Ferrari

+33% for Richemont

+12% for LVMH

+18% for Kering

This performance has significantly contributed to the strong start for the European stock market, particularly in France. The rebound in Kering’s stock is especially noteworthy, suggesting the market believes the company has reached its bottom. However, the real test will be whether performance improves going forward. If not, the decline could be steep for shareholders.

If you enjoyed this article and like Quality Stocks, please give it a like and spread the word!

While this newsletter provides valuable content for free subscribers, here is why upgrading to a paid subscription is worth it:

Access exclusive content. Dive deeper with detailed analyses, advanced insights, and premium research not available to free subscribers

Follow my portfolio. Gain exclusive access to my portfolio, including monthly updates, tracking my moves, and watchlists

Discover more stock ideas. Explore in-depth stock ideas, technical analyses, and strategies tailored to uncover hidden opportunities

Support this newsletter. Your subscription directly supports the creation of high-quality, valuable content to help you achieve your investment goals