Alphabet's Q1 2025 earnings report: showing strength

What you need to know about Alphabet's Q1

Alphabet was the first among the Magnificent 7 to report earnings, acting as a beacon amidst a turbulent market. Far from fading, the company demonstrated remarkable momentum.

For context, here is my previous analysis of Alphabet from the "Stock of the Week" series, where I highlight companies experiencing significant news flow or presenting compelling price-to-fundamental dynamics, whether positive or occasionally negative.

My analysis was that the prevailing market sentiment (fueled by concerns over potential market share losses in Google Search) was likely too pessimistic. Given Alphabet's long-term potential and its capacity to expand margins, the outlook seemed more favorable than the market was pricing in. From a technical standpoint, the stock also appeared to be well-supported around the $150 level.

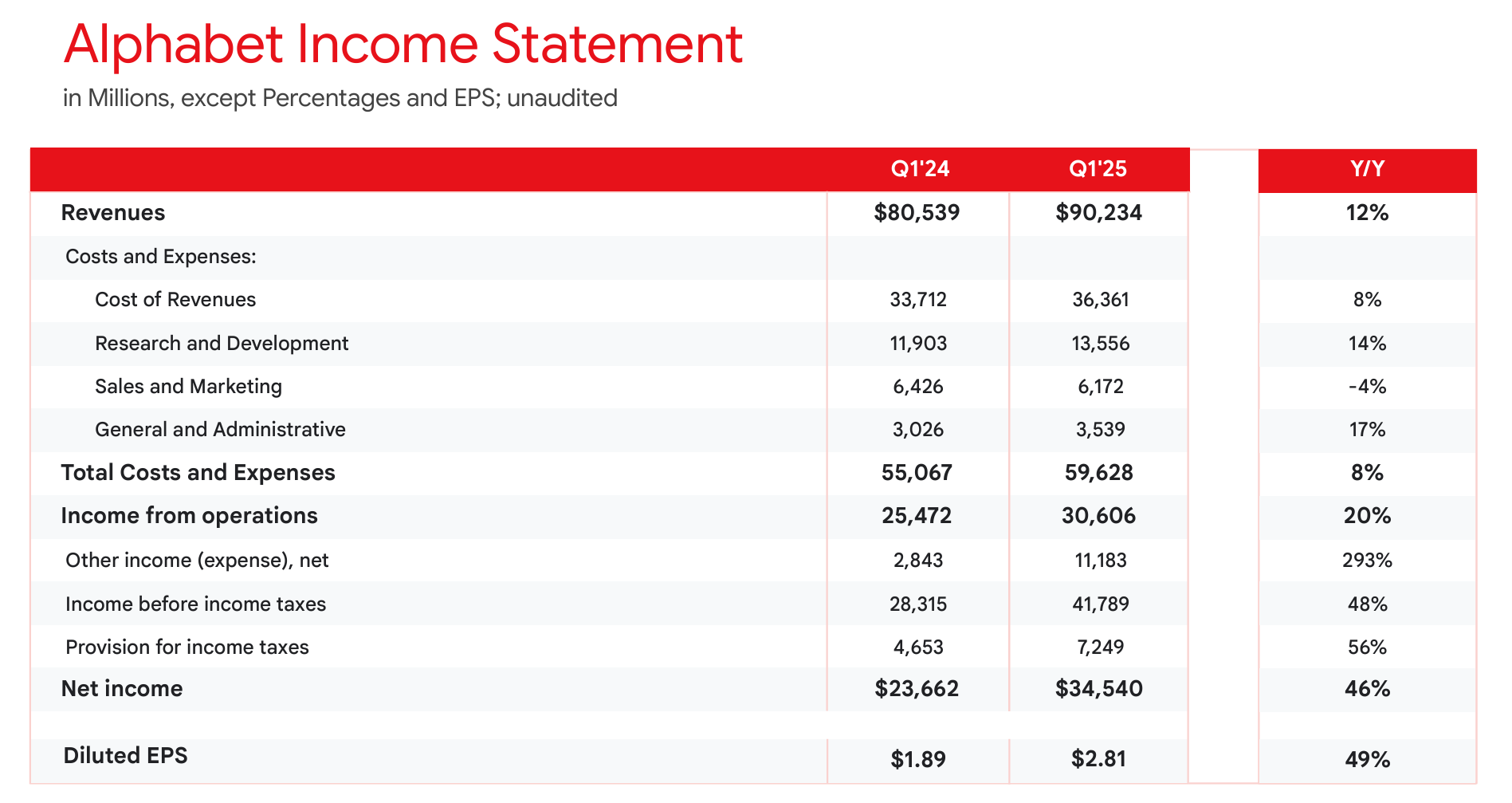

Earnings snapshot

Details

First, it is important to clarify the headline EPS growth. While a 49% increase may seem impressive, it was significantly inflated by approximately $8B in unrealized gains from an investment in a private company, possibly SpaceX.

Operating margin expanded, pointing to around 20% growth. When factoring in share buybacks, a normalized EPS growth closer to 22% seems reasonable. That is a solid performance for a company trading at roughly 18x earnings.

This strong performance was driven in part by a modest 9% increase in operating expenses, underscoring disciplined cost management.

Breaking it down by segment, YoY growth looked as follows:

Google Services

Google Search +10% YoY

YouTube Ads +10% YoY

Google Network –2% YoY

Subscriptions, Platforms & Devices +19% YoY

Google Cloud +28% YoY

CAPEX and Free Cash Flow

Free cash flow grew modestly, up 13% YoY and 8% TTM. This more tempered growth is largely a result of the company’s significant increase in capital expenditures, which rose 43% YoY, driven by investments in Cloud, AI, and Waymo.

As I noted in a previous article, I see these elevated CAPEX levels not as a red flag, but as a strategic move to support long-term growth. While they do weigh on free cash flow in the short term and introduce additional risk, they also position the company for future upside.

Business highlights

Growth in Cloud remains strong with Google Cloud revenues increasing 28% to $12.3B, led by growth in Google Cloud Platform (GCP) across core GCP products, AI Infrastructure, and Generative AI Solutions

Paid subscriptions across Youyube and Google One have topped 270 million

Waymo’s self-driving taxi service is delivering more than 250,000 paid rides each week in the US. That is up 5 times from a year ago

AI is still a strong focus with the roll out of Gemini 2.5 “which is achieving breakthroughs in performance and is an extraordinary foundation for [the] future innovation”. Alphabet aimed to turn AI into a platform and not just a feature

Search paid click revenue also grew, though primarily driven by higher prices. The number of paid clicks rose by just 2%, which could indicate a potential future slowdown, a trend that was expected and likely at least partially priced in. New AI features to make Search smarter could help regain momentum

Meanwhile, the company continues to face significant legal challenges, including the ongoing search monopoly trial, the ad tech monopoly ruling, the Play Store antitrust appeal, and increased scrutiny under the EU Digital Markets Act

YouTube continues to grow, expanding its market share. In the US, YouTube now captures 12% of total TV viewing time, compared to 8% for Netflix. This marks a significant shift, as the two platforms were tied just 18 months ago

A gift for the shareholders

Alphabet also announced a 5% dividend increase and an impressive $70B share buyback program. This move comes as a slight surprise, given the company’s substantial capital expenditure requirements and recent strategic acquisitions, such as the $32B purchase of cybersecurity firm Wiz.

However, it sends a clear message: management is confident in Alphabet’s ability to generate long-term value and believes the current stock price presents an attractive opportunity to buy back shares aggressively.

We will have to wait and see how it plays out!

How do you view Alphabet’s latest earnings results?